Research

Weekly Market Recap - November 2, 2025

The Federal Reserve cut rates by 25 bps to support slowing growth, prompting a cautious market response. Crypto markets fell as regulatory delays and macro uncertainty drove investors toward stable, yield-based assets.

Download the PDF

Estimated Reading Time: 11 minutes

Summary

The Federal Reserve lowered its benchmark rate by 25 basis points to a range of 3.75%-4.00%, marking the first cut in three years as policymakers sought to support growth amid signs of a cooling labor market and persistent inflation. However, officials signaled caution about further easing, emphasizing that upcoming data on inflation and employment will guide future decisions. Broader markets responded with measured optimism - equities advanced modestly, Treasury yields edged higher, and the U.S. dollar strengthened, reflecting balanced investor sentiment.

In digital assets, the market declined amid a mix of macroeconomic and structural pressures, rather than simple profit-taking. The total crypto market capitalization fell 1.52% as risk sentiment weakened following renewed concerns about the Federal Reserve's monetary policy path and delays in regulatory approvals for several anticipated crypto ETF products. These factors triggered a wave of liquidations in leveraged positions, particularly in altcoins, leading investors to rotate toward larger, more liquid assets such as Bitcoin and Ethereum, which together continued to represent over 70% of total market value. Despite the downturn, stablecoins remained steady at $307.5 billion, underscoring their role as liquidity anchors within the ecosystem, while tokenized real-world assets (RWAs) advanced to $34.6 billion, supported by institutional inflows into U.S. Treasury-backed and yield-bearing instruments.

On the regulatory front, the Australian Securities and Investments Commission (ASIC) clarified licensing requirements for digital asset products, while the U.S. saw a wave of new exchange-traded funds (ETFs) - including Bitwise's Solana Staking ETF and Grayscale's GSOL - reflecting stronger institutional demand for diversified crypto exposure. In Japan, the launch of the JPYC yen-pegged stablecoin marked a milestone for regulated fiat-backed tokens.

In technology and innovation, major players accelerated blockchain adoption: Visa expanded support for four stablecoins across multiple chains; PayPal partnered with OpenAI and Google to embed AI-driven payments; and Circle launched the public testnet of its Arc Layer-1 blockchain, backed by over 100 institutional partners.

Market Confidence and Adoption

Broad Markets

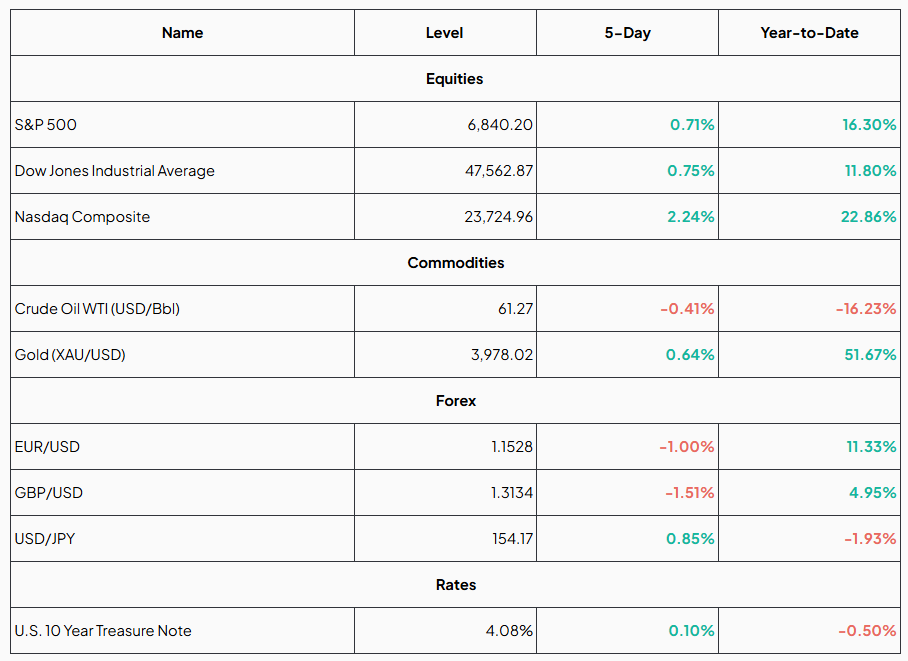

Equity markets advanced modestly over the week, supported by improved risk sentiment following steady macroeconomic signals.

The Nasdaq Composite led gains with a 2.24% rise, extending its 22.86% year-to-date rally, while the S&P 500 and Dow Jones Industrial Average climbed 0.71% and 0.75%, respectively, reflecting continued strength in large-cap and technology stocks.

In commodities, WTI crude oil eased 0.41% to $61.27 per barrel, deepening its 16.23% year-to-date loss, whereas gold advanced 0.64% to $3,978.02, maintaining its role as a defensive asset with an impressive 51.67% gain for the year.

In foreign exchange markets, the euro and pound weakened against the U.S. dollar, falling 1.00% and 1.51%, respectively, while USD/JPY rose 0.85%, signaling renewed dollar strength.

Meanwhile, U.S. Treasury yields edged higher, with the 10-year note increasing 0.10 percentage points to 4.08%, reflecting cautious optimism amid shifting interest rate expectations.

Weekly Market Data

Source: MarketWatch.com , Google Finance, TradingView (As of November 2, 2025)

Cryptocurrencies

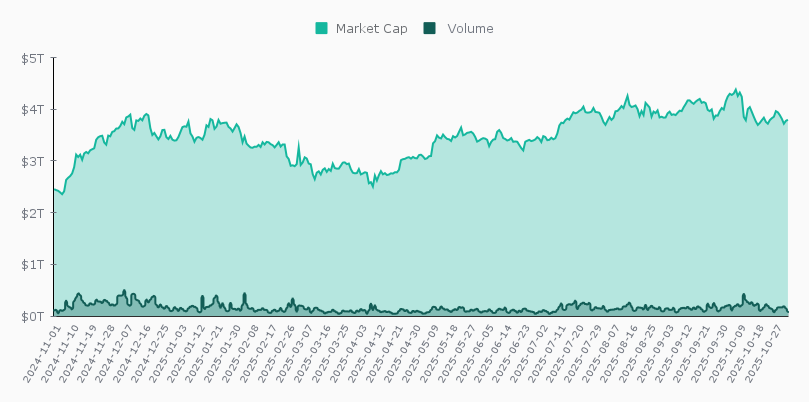

From October 27 to November 2, 2025, the total crypto market cap slipped 1.52%, swinging between a weekly high of about $4 trillion (Oct 27) and a low near $3.72 trillion (Oct 31) before ending around $3.8 trillion. Trading activity rose 5.33% over the same period to roughly $81.6 billion, signaling a modest pickup in participation even as prices softened.

This movement appears partly influenced by broader macroeconomic sentiment linked to the Federal Reserve's policy outlook. While the Fed did not announce a major policy change during that week, ongoing expectations of a "higher-for-longer" interest rate stance continued to weigh on risk assets, including cryptocurrencies. Investors showed signs of caution, leading to profit-taking and portfolio rebalancing, particularly after earlier gains in large-cap tokens. The simultaneous rise in trading volume suggests that market participants were actively repositioning ahead of potential monetary developments, contributing to short-term volatility.

Overall, the week reflected a consolidation phase shaped by macro uncertainty, rather than a deep structural decline in the crypto market.

Crypto Market Capitalization and Volume

Source: CoinGecko.com

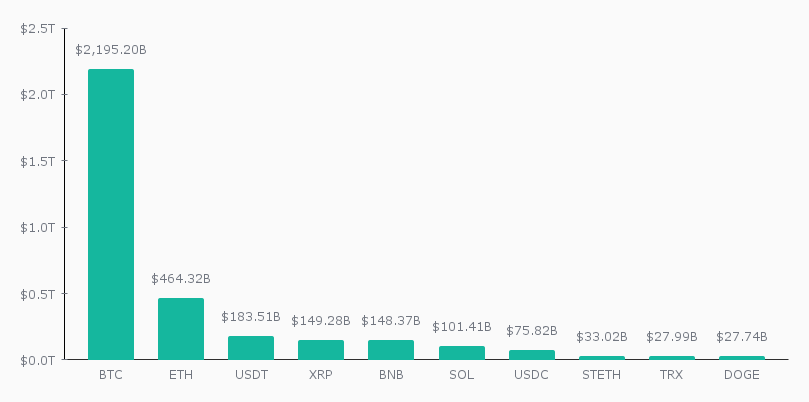

Bitcoin (BTC) continues to dominate the cryptocurrency market with a capitalization of $2.20 trillion (58.1%), maintaining a strong lead over Ethereum (ETH), which holds $464.3 billion (12.3%). Stablecoins Tether (USDT) and USD Coin (USDC) remain key pillars of liquidity, representing 4.9% and 2.0% of the market, respectively. XRP and BNB are nearly tied in market value at around $149 billion each, jointly accounting for 7.8% of total capitalization. Solana (SOL) follows with $101.4 billion (2.7%), while Lido Staked Ether (stETH), TRON (TRX), and Dogecoin (DOGE) round out the top ten with market shares below 1% each. Overall, the market remains heavily concentrated in Bitcoin and Ethereum, which together comprise more than 70% of the total crypto capitalization.

Cryptocurrency Market Share

Source: CoinGecko.com (As of November 2, 2025)

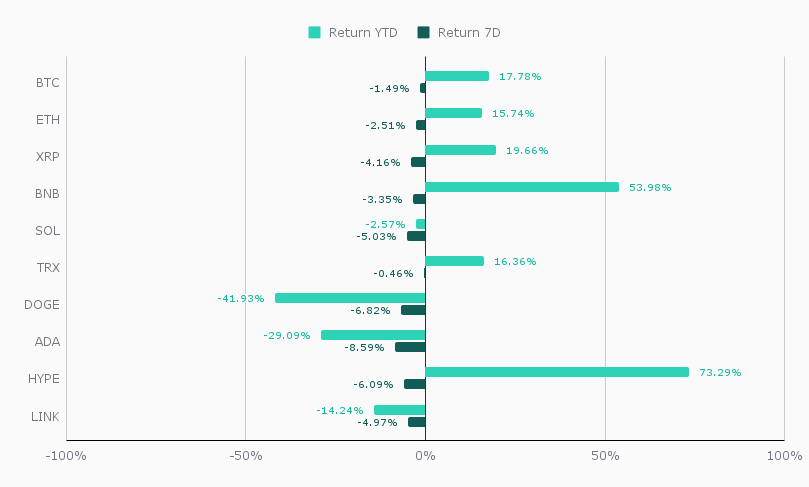

The crypto market saw a broad pullback during this week, with most major assets posting negative returns. Bitcoin (BTC) slipped 1.49% to around $109,889, while Ethereum (ETH) dropped 2.51% to approximately $3,852. Among large-cap altcoins, Solana (SOL) led the declines with a 5.03% weekly loss, and Cardano (ADA) fell even further, down 8.59% to $0.60. Dogecoin (DOGE) also tumbled 6.82%, extending its steep year-to-date decline of more than 41%.

Weekly Return of the Top 10 Cryptocurrencies by Market Capitalization (excluding Stablecoins)

Source: TradingView.com (As of November 2, 2025)

Stablecoins

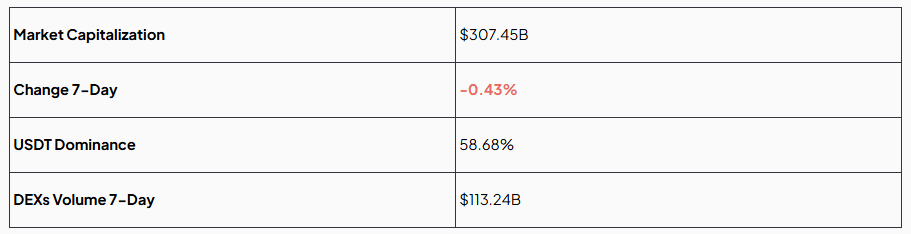

Despite their recent upward trend, stablecoins saw their total market capitalization decline to nearly $307.5 billion this week, according to DefiLlama.

The stablecoin market remains largely stable, reflecting a continuation of existing trends across major networks rather than major structural shifts. Ethereum remains the clear leader, with its stablecoin market cap reaching a new all-time high of $165.28 billion, up 1.33% week-over-week and accounting for roughly 52% of the total stablecoin supply - reaffirming its dominance in decentralized finance. TRON follows with about $78.73 billion in stablecoins, primarily Tether (USDT), maintaining a strong position in transaction volume and user activity, though its share slipped 0.11%, suggesting mild competitive pressure from other networks. Meanwhile, Solana continues to attract investor attention, posting a 0.06% increase in stablecoin value to around $14.6 billion, consistent with its broader momentum in on-chain activity.

Looking at individual assets, Tether (USDT) accounts for 59.68% of the total stablecoin market, valued at $183.48 billion, reflecting a 0.22% increase over the week. USD Coin (USDC) follows with a market capitalization of $75.39 billion, representing 24.52% of the stablecoin market and marking a 0.63% decline over the same period.

Overall, the data indicate a stable, consolidating phase for the stablecoin market, with little change in network dominance or asset distribution.

Key Metrics

Source: DefiLlama.com (As of November 2, 2025)

Tokenized Real-World Assets (RWA)

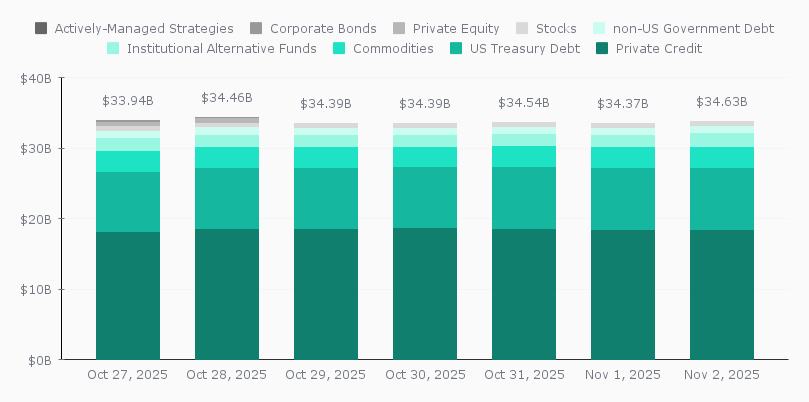

As of November 2, 2025, the total value of tokenized real-world assets (RWAs) on-chain stood at approximately $34.63 billion, marking a 2.79% increase from the previous week's levels. Private credit remained the dominant category with $18.44 billion, accounting for over half of the total market, followed by U.S. Treasury debt, which climbed to $8.73 billion amid sustained demand for yield-bearing, regulated instruments. Commodities-largely gold-backed tokens-rose slightly to $2.97 billion, while institutional alternative funds saw a notable uptick of 10.41%, reaching $1.95 billion, driven by renewed institutional participation. Other categories such as non-U.S. government debt, stocks, and corporate bonds remained relatively stable. Overall, the week reflected a steady expansion of the tokenized asset market, with capital continuing to concentrate in private credit and Treasury-backed products as investors favored on-chain exposure to traditional yield-generating instruments.

Total Tokenized Real-Word Assets Onchain

Source: RWA.xyz (As of November 2, 2025)

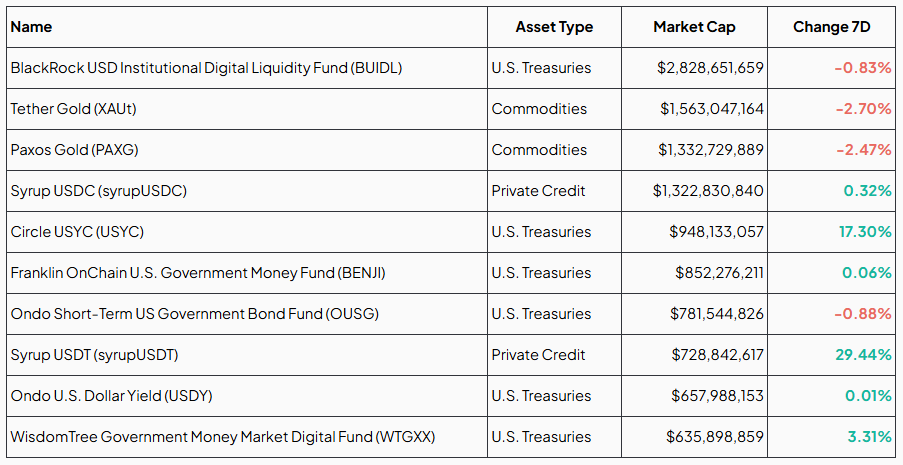

Top Ten Tokenized RWA

The tokenized asset market this week was marked by mixed performance across categories, led by continued institutional traction in U.S. Treasuries-backed products. BUIDL remained the largest tokenized fund with a market cap of $2.83 billion, though it dipped 0.83% over the week. In contrast, Circle's USYC saw strong growth, surging 17.3% to $948 million, highlighting rising demand for on-chain Treasury exposure. Among newer entrants, Syrup USDT recorded an impressive 29.44% weekly jump to $729 million, reflecting growing investor interest in private credit-backed assets. Meanwhile, commodity-backed tokens such as Tether Gold (XAUt) and Paxos Gold (PAXG) declined 2.7% and 2.47%, respectively, as gold-linked assets softened alongside broader market caution. Overall, the segment continues to show a clear preference for regulated U.S. Treasury products.

Source: RWA.xyz (As of November 2, 2025)

Macroeconomic Factors

Key Takeaways

U.S. Fed lowers short-term rates; further cuts uncertain

The Federal Open Market Committee (FOMC) lowered the federal funds rate target by 25 basis points to a range of 3.75%-4.00%, its lowest level in three years, aiming to support the economy amid signs of a cooling labor market and lingering inflation.

Fed Chair Jerome Powell emphasized that a follow-up rate cut in December is "far from guaranteed", highlighting divisions within the committee and uncertainty surrounding the economic outlook. Policymakers indicated that while they could cut rates again if the labor market weakens significantly, they remain ready to raise rates if inflationary pressures resurface.

The Fed also noted that the ongoing government shutdown has delayed key economic data, making upcoming reports on inflation and employment crucial for shaping future policy decisions.

U.S. consumer confidence slips in October

The Conference Board's Consumer Confidence Index fell to 94.6 in October from 95.6 in September, marking its lowest level in six months. The decline reflects growing concerns about job availability and future economic conditions, even as assessments of current business and labor markets improved slightly.

Persistent inflation and uncertainty around the labor market continue to weigh on sentiment, reinforcing views that the U.S. economy may be slowing and adding pressure on the Federal Reserve as it considers its next policy moves.

Bank of Canada reduces policy rate; signals pause in easing

The Bank of Canada lowered its target overnight interest rate by 25 basis points to 2.25%, marking a second consecutive cut and the lowest level since July 2022.

Governor Tiff Macklem signaled that the Bank of Canada may pause further rate cuts, noting that the current level is appropriate to keep inflation near 2% unless economic conditions worsen.

Eurozone GDP grows modestly in Q3, signaling fragile recovery

The euro area's economy expanded by a modest 0.2% in the third quarter (Q3) of 2025, slightly above market expectations and suggesting a fragile but continuing recovery across the bloc. The preliminary estimate, released by Eurostat, points to mild growth amid persistent structural headwinds, including weak investment and subdued consumer demand.

While the positive figure indicates the region avoided stagnation, it underscores the eurozone's ongoing struggle to regain momentum following months of sluggish performance. Economists note that uncertainty in global trade, elevated borrowing costs, and muted industrial output continue to constrain growth, adding pressure on the European Central Bank to balance inflation control with the need to support economic expansion.

ECB keeps key interest rate at 2%

The European Central Bank held its deposit facility rate steady at 2 % in its October meeting, marking the third consecutive session with no change in borrowing costs.

The decision reflects the ECB's recognition that although inflation is near its target and the economy grew modestly, significant uncertainties remain. These include trade tensions, a strong euro, weak investment and differential performance across member states - factors that keep the bank cautious despite the improved inflation outlook.

Markets now expect the ECB to take a "meeting-by-meeting" approach going forward, with future rate changes conditional on fresh data rather than on a preset path.

Bank of Japan holds rate at 0.5%, gauges wage momentum for next move

The Bank of Japan decided in its October meeting to maintain the policy rate at 0.50%, in line with market expectations and continuing its cautious stance amid mixed signals in the economy.

Governor Kazuo Ueda emphasised that while inflation has remained above the 2% target and the economy is showing signs of recovery, the timing of a rate hike will depend on stronger wage momentum and more definitive data.

The bank's decision suggests it is transitioning away from ultra-accommodation, yet remains reluctant to act prematurely. The yen weakened on the announcement, highlighting market concern that the BoJ may lag behind global peers in tightening.

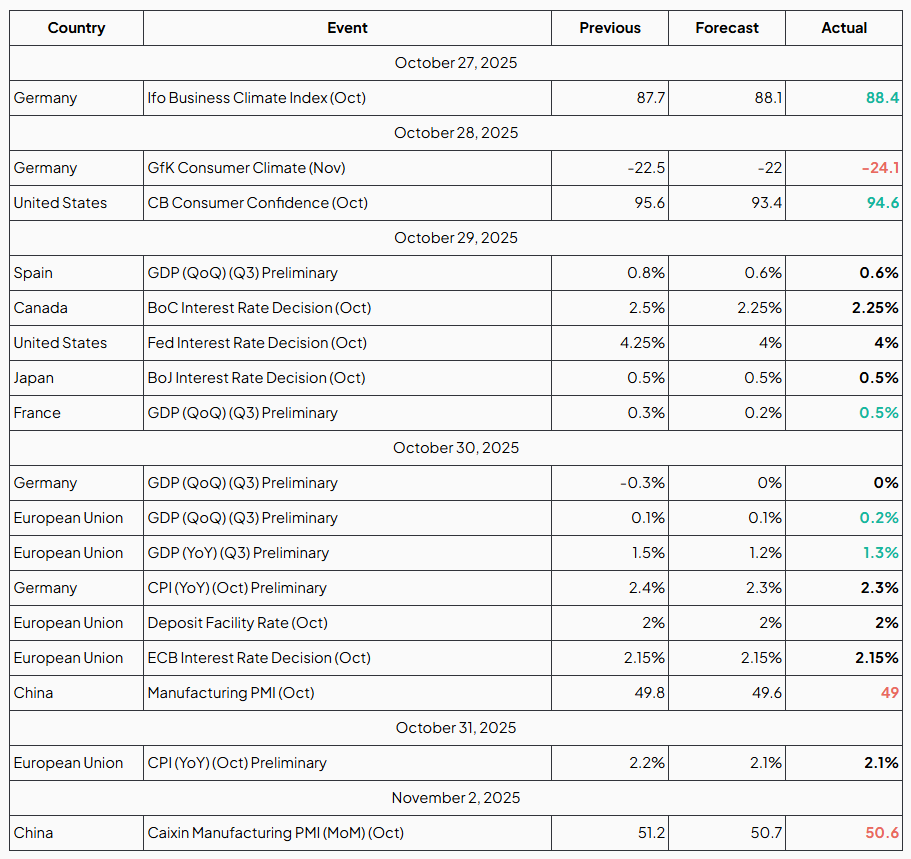

China's manufacturing PMI signals continued weakness

China's manufacturing sector showed further signs of strain in October 2025, with the official Purchasing Managers' Index (PMI) slipping to 49.0 from 49.8 in September - marking the seventh straight month of contraction. The decline reflects persistent weakness in output, new orders, and export demand, as global trade conditions remain sluggish and domestic demand softens. A separate private survey by S&P Global reported a PMI of 50.6, indicating marginal expansion but also a slowdown from the previous month. Rising input costs and falling output prices are pressuring manufacturers' profit margins, underscoring the challenges facing China's industrial recovery despite limited government support measures.

Week's Overview

Source: Investing.com

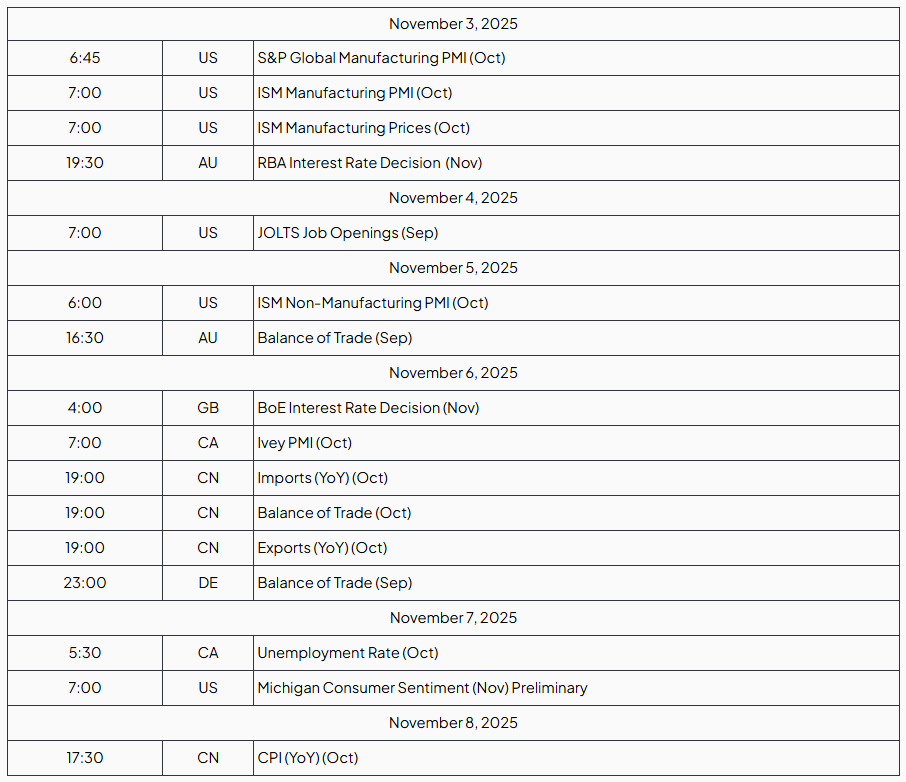

The Week Ahead

Next week, market attention will center on U.S. business activity and labor market data - including the ISM PMIs and the JOLTS Job Openings report - while rate decisions from the Reserve Bank of Australia and Bank of England will be closely watched for guidance on future policy direction

Source: Investing.com Time: (GMT/UTC - 8h)

Regulation Environment

Australia's financial regulator releases updated guidance on digital assets

The Australian Securities and Investments Commission (ASIC) has published a revised version of Information Sheet 225, clarifying when digital asset products and services are likely to be considered financial products under the Corporations Act.

The guidance explains that certain digital assets - including stablecoins, tokenised products, and staking services - are likely to require an Australian Financial Services Licence (AFSL), while Bitcoin and some non-fungible tokens (NFTs) are not considered financial products under the current framework.

To support a smooth transition, the regulator has introduced a "no-action" relief period until June 2026, allowing firms time to align their operations with the new requirements.

Bitwise launches first U.S. Solana Staking ETF ($BSOL)

Solana's ecosystem takes a significant step into mainstream investment markets as Bitwise has introduced the BSOL fund - the first U.S. exchange-traded product (ETP) to offer 100% direct exposure to Solana's spot price while also staking all its holdings to capture yield.

The new fund will deploy an innovative structure: it partners with Helius Labs to run the staking operations, aiming to stake 100% of its SOL holdings and deliver the network's approximately 7% average staking reward rate back to the fund. Initially, the fund's management fee is set at 0% for the first three months (on the first $1 billion in assets) and subsequently moves to 0.2%.

The launch comes amid strong investor demand: on its first day of trading the fund attracted around $223 million in assets, signaling significant institutional interest and marking a milestone for staking-based crypto investment vehicles in the U.S.

Grayscale debuts Solana ETF, joining Bitwise in the SOL-staking ETP race

Grayscale Investments has launched its staking-enabled Solana fund, trading under the ticker GSOL on the NYSE Arca, marking the company's entry into the U.S. regulated market for spot crypto products with integrated staking capability.

The vehicle launched with over $100 million in assets under management (AUM) and enables investors to earn network staking rewards directly through the fund structure.

While the annual management fee is set at 0.35%, GSOL faces growing competition from Bitwise's BSOL, which offers similar Solana exposure at a lower cost.

JPYC Inc. launches Japan's first Yen-denominated stablecoin

Japan has taken a major step by launching its first fully regulated yen-pegged stablecoin, JPYC, issued by JPYC Inc. The token is pegged 1:1 to the Japanese yen and is backed by yen deposits and Japanese government bonds.

The launch comes under Japan's updated regulatory framework (the amended Payment Services Act) which classifies certain fiat-backed tokens as "electronic payment instruments" and requires regulated issuance.

Litecoin (LTC) and Hedera (HBAR) ETFs debut on Wall Street

Canary Capital has launched the first U.S. exchange-traded funds (ETFs) linked to Litecoin (LTC) and Hedera (HBAR), marking a milestone in the expansion of regulated crypto investment products beyond Bitcoin and Ethereum.

The Hedera ETF, trading under the ticker HBR on the Nasdaq, offers institutional investors direct exposure to HBAR's spot price, while the Litecoin ETF provides similar access through a regulated, custody-backed structure.

The approval and launch of these funds highlight the U.S. Securities and Exchange Commission's (SEC) evolving openness toward diversified digital asset products, signaling growing institutional acceptance of alternative cryptocurrencies within mainstream financial markets.

Technology and Innovation

Visa Inc. to support payments in four stablecoins across four blockchains

Visa is expanding its digital-asset payments infrastructure by enabling support for four major stablecoins across four distinct blockchain networks, offering seamless conversion into traditional fiat currencies.

The initiative covers stablecoins including USD Coin (USDC), Euro Coin (EURC), PayPal USD (PYUSD) and Global Dollar (USDG), operating on the blockchains of Ethereum, Solana, Stellar, and Avalanche.

Visa's CEO stated that the expanded support will allow more than 25 fiat currencies to be converted via the network, reinforcing Visa's ambition to act as a bridge between traditional fiat payments and blockchain-based stablecoin transactions.

PayPal partners with OpenAI and Google to drive the next wave of AI-powered payments

PayPal has announced major partnerships with OpenAI and Google, positioning itself at the forefront of AI-driven digital commerce. The collaboration with OpenAI integrates PayPal's digital wallet directly into ChatGPT, enabling users to make purchases and complete transactions seamlessly within the chat interface - a move that transforms conversational AI into a fully interactive shopping platform.

At the same time, PayPal's alliance with Google will embed its payment infrastructure across Google's ecosystem, from Search and Cloud to Android and YouTube, while jointly developing AI-powered payment and commerce solutions.

These partnerships mark a pivotal step toward the rise of agentic commerce, where AI not only recommends products but also executes purchases, signaling a new era in the convergence of artificial intelligence, payments, and digital consumer experiences.

Circle Internet Group launches public testnet of "Arc" layer-1 blockchain with 100+ institutional partners

Circle has officially rolled out the public testnet for Arc, its open Layer-1 blockchain designed for enterprise use in stablecoins, payments, FX and tokenised assets. The launch features participation from over 100 companies across finance, technology and payments - including BlackRock, Visa, Amazon Web Services (AWS), and Anthropic.

Arc is built to provide predictable dollar-based fees, sub-second transaction finality and optional configurable privacy, while integrating directly with Circle's full-stack platform and its USDC stablecoin.

The breadth of institutional backing signals a major step toward bridging traditional financial infrastructure with on-chain innovation, as Circle positions Arc as a foundational economic operating system for the internet.

Standard Disclaimer: This report is provided for informational purposes only and does not constitute legal, financial, or investment advice. The views expressed represent the author's perspective at the time of publication and may change as market conditions develop. Although the information is drawn from sources deemed reliable, its accuracy and completeness are not guaranteed. Readers should exercise their own judgment and perform due diligence before making any decisions based on this report.

Contributors

Ana CabaleiroFinancial Analyst