Research

Weekly Market Recap - November 9, 2025

Global markets came under pressure this week as tech stocks led a correction and safe-haven demand strengthened; simultaneously, cryptocurrencies tumbled on institutional outflows and macro uncertainty, reinforcing a risk-off tone across asset classes.

Download the PDF

Estimated Reading Time: 25 minutes

Summary

Global markets ended the week under pressure as investors reassessed growth prospects and central bank signals. U.S. equities retreated from record highs, with profit-taking concentrated in large-cap technology and AI names. The narrowing breadth of the rally raised concerns about sustainability, while oil extended its slide below $60 on weaker demand expectations. Gold climbed toward $4,000 as investors sought safety, and Treasury yields held steady around 4.1%, reflecting cautious sentiment amid persistent inflation and mixed macro data.

In digital assets, the market faced a pronounced correction as Bitcoin fell to multi-month lows and recorded heavy outflows from institutional products and exchanges. The sell-off was amplified by leveraged liquidations and a broader shift toward risk reduction across global markets. Ethereum and major altcoins followed lower, though overall capitalization remained above $3.5 trillion. Stablecoins held steady near $305 billion, underscoring their role as liquidity anchors, while tokenized real-world assets (RWAs) advanced modestly as investors favored on-chain Treasury and credit exposure for yield and stability.

Regulatory progress accelerated across major markets, signaling a shift toward greater institutional integration of digital assets. In the United States, Ripple launched Ripple Prime, a regulated digital-asset prime brokerage offering trading, financing, and clearing services for institutional clients, marking the company's formal entry into the U.S. market and expanding its footprint beyond blockchain payments. In Europe, Kraken enabled the use of cryptocurrencies as collateral for derivatives trading under the MiFID II framework, becoming one of the first platforms to bridge regulated finance with on-chain collateral models. Meanwhile, Hong Kong reinforced its leadership in digital-asset policy as Franklin Templeton introduced a tokenized U.S. dollar money-market fund for professional investors, reflecting growing regulatory clarity around tokenized securities. Together, these initiatives underscore a regulatory landscape that is evolving toward compliance-driven innovation, with global frameworks increasingly supporting institutional participation and real-world asset tokenization.

Technological and institutional innovation accelerated across the ecosystem. Fireblocks, Solana, TON, Polygon, and Stellar formed the Blockchain Payments Consortium to establish unified crypto-payment standards. Tangem introduced Tangem Pay, enabling on-chain USDC spending through Visa, and Google integrated prediction-market data from Polymarket and Kalshi directly into search results. RedStone launched Credora, delivering dynamic risk ratings for DeFi lending, while leading Ethereum protocols created the EPAA to ensure that on-chain infrastructure has a policy voice. These advancements highlight a maturing phase for blockchain technology, one centered on interoperability, institutional readiness, and tangible real-world use cases rather than experimentation alone.

Market Confidence and Adoption

Broad Markets

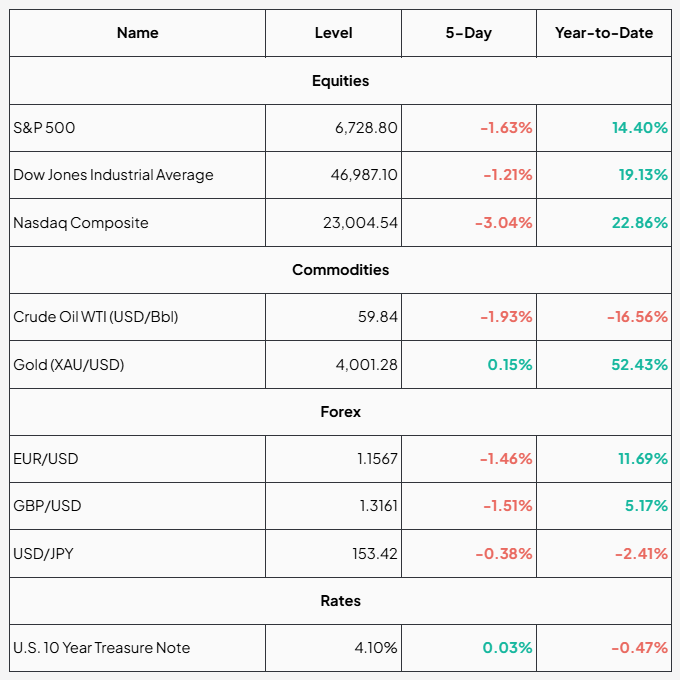

Global markets saw a mixed week as investors digested shifting economic data and the concentrated leadership of U.S. equities. Tech and AI giants continued to dominate sentiment, while commodities and forex markets reflected a more cautious global stance.

After a strong start to November, U.S. equity markets cooled as investors took profits from a powerful rally led by large-cap technology stocks. The Nasdaq Composite, heavily weighted toward AI-related and high-growth companies, fell over 3% - its sharpest pullback since April. The S&P 500 and Dow Jones also slipped modestly, though they remain near record territory. Analysts noted that the rally has become increasingly narrow, driven by a handful of mega-cap names like Amazon and Nvidia. Broader market participation remained weak, raising concerns about the rally's sustainability.

Crude oil prices dropped below $60 a barrel, marking another week of declines amid concerns over slowing global demand and steady production levels. With the U.S. dollar strengthening and energy consumption softening in Asia, the pressure on oil markets persisted.

In contrast, gold continued to climb, briefly touching the $4,000 mark. The metal's strength underscores its role as a hedge against uncertainty. Stable Treasury yields and ongoing geopolitical tensions supported demand even as risk assets like tech stocks dominated headlines.

The U.S. dollar strengthened modestly against major currencies as investors sought safety amid choppy equity trading. The euro and pound each lost around 1.5%, reflecting renewed caution in global risk appetite. Meanwhile, the Japanese yen hovered near ¥153 per USD, with a slight rebound as U.S. yields eased and interest-rate differentials narrowed.

The U.S. 10-Year Treasury yield held steady near 4.1%, fluctuating only modestly through the week. Investors balanced softer labour-market data against expectations that the Federal Reserve will maintain higher rates for longer. The relatively flat yield curve suggests that bond traders are waiting for clearer economic signals, with inflation showing signs of moderation but growth data remaining mixed.

Weekly Market Data

Source: MarketWatch.com , Google Finance, TradingView (As of November 9, 2025)

Cryptocurrencies

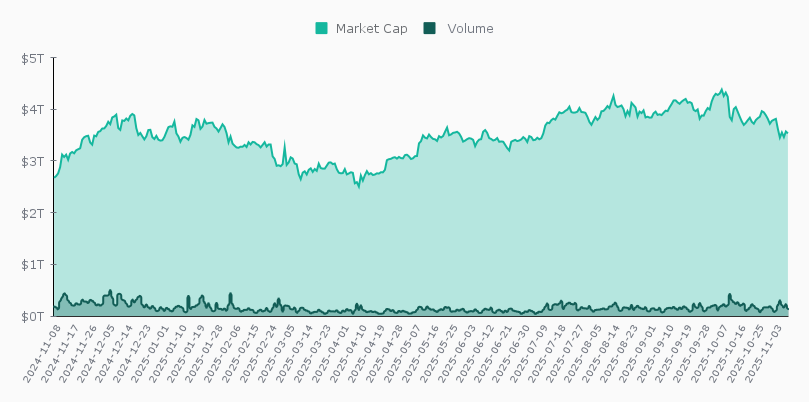

The cryptocurrency market experienced a volatile and corrective week, as traders took profits following strong October gains. Total market capitalization declined from early highs to settle near $3.5 trillion, while trading volumes surged mid-week, signaling heightened activity amid sell-offs and position adjustments.

Market data shows that the sharpest moves occurred midweek, when trading volume spiked above $300 billion, reflecting widespread liquidations of leveraged positions and short-term risk-off sentiment. Analysts attributed the pullback to cooling momentum after a period of rapid appreciation, coupled with broader uncertainty in global markets.

Despite the drop, prices began stabilizing toward the weekend, and by Sunday capitalization had partially recovered. Most analysts view the downturn as a healthy correction rather than a structural reversal, with long-term optimism persisting around blockchain innovation and the integration of AI technologies in the digital asset space.

In summary, the week underscored a market in consolidation mode, cooling from record highs but maintaining resilience, as investors adjust exposure ahead of potential macroeconomic catalysts later in the month.

Crypto Market Capitalization and Volume

Source: CoinGecko.com

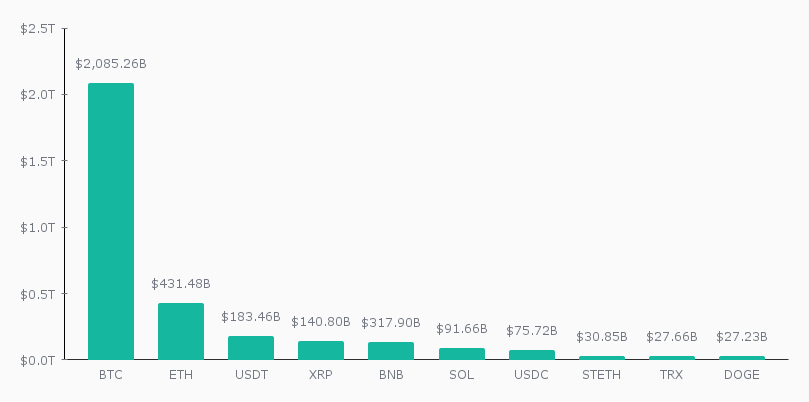

The cryptocurrency market experienced a general contraction this week, with declines across most major assets while overall dominance patterns remained relatively stable. Bitcoin (BTC) retained its leadership position with a market capitalization of $2.09 trillion, representing 57.6% of the total market, slightly down from 58.1% last week. Ethereum (ETH) followed with $431.5 billion in capitalization (11.9% share), reflecting a comparable decline in both value and dominance.

Among stablecoins, Tether (USDT) and USD Coin (USDC) demonstrated relative resilience. Tether's market cap remained near $183.5 billion, with its market share increasing from 4.9% to 5.1%, while USDC held steady around $75.7 billion, gaining a slight 0.1 percentage point in share to reach 2.1%.

Mid-tier assets such as XRP and BNB both saw declines in capitalization, down to $140.8 billion and $137.9 billion, respectively, maintaining a combined market share of roughly 7.7%. Solana (SOL) also eased from $101.4 billion to $91.7 billion, reducing its share from 2.7% to 2.5%, signaling softer investor sentiment.

Further down the rankings, Lido Staked Ether (stETH) slipped to $30.9 billion, TRON (TRX) to $27.7 billion, and Dogecoin (DOGE) to $27.2 billion, each holding less than 1% of the total market. Despite the broad pullback, market concentration remains pronounced, with Bitcoin and Ethereum together commanding nearly 70% of total cryptocurrency capitalization, underscoring their continued dominance amid fluctuating market conditions.

Cryptocurrency Market Share

Source: CoinGecko.com (As of November 9, 2025)

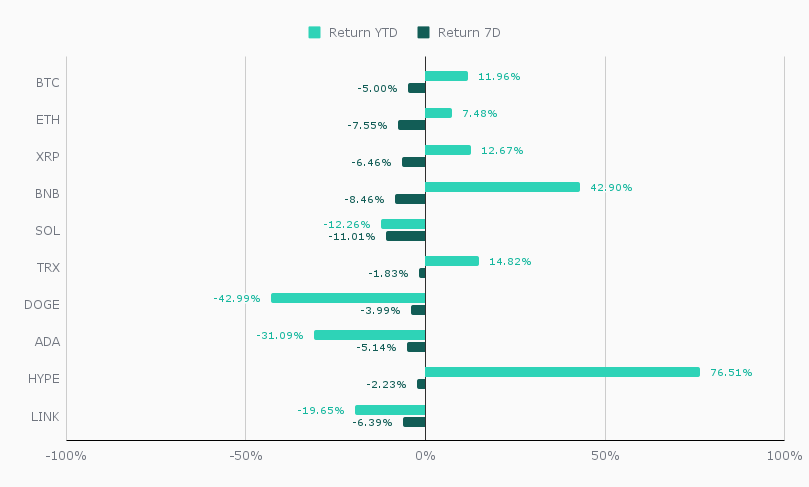

The cryptocurrency market entered a correction phase this week, as risk-off sentiment swept through digital assets following macroeconomic uncertainty and heavy leveraged liquidations. Despite the pullback, most major cryptocurrencies held on to their broader-year gains, reflecting underlying strength beneath short-term volatility.

Bitcoin (BTC) led the market downturn, slipping 5% over the week to $104,545, after briefly testing higher resistance levels earlier in November. Analysts attributed the decline to overleveraged long positions being flushed out, along with renewed caution following signals from the Federal Reserve that interest-rate cuts could be delayed.

Ethereum (ETH) fell 7.6% to $3,578, tracking Bitcoin's weakness amid broader selling pressure. Despite strong developer activity and progress on its scaling roadmap, ETH's short-term performance was muted by market-wide liquidations and tighter liquidity conditions.

Altcoins suffered steeper losses, with Solana (SOL) down 11% to $165.69, BNB dropping 8.5% to $1,001.46, Cardano (ADA) falling 5.1% to $0.58, and Chainlink (LINK) sliding 6.4% to $16.05. These moves reflect the tendency of altcoins to amplify Bitcoin's directional swings during periods of market stress.

Among mid-cap assets, TRON (TRX) proved more resilient, slipping only 1.8% to $0.29, supported by steady network growth and stable DeFi demand. Dogecoin (DOGE) eased 4% to $0.18, continuing its weak trend this quarter as speculative interest faded. In contrast, Hyperliquid (HYPE) demonstrated relative strength, edging down just 2.2% to $42.27, buoyed by strong exchange traction and investor enthusiasm for emerging DeFi infrastructure.

Overall, the market's declines align with a broader wave of risk aversion triggered by macroeconomic caution, regulatory developments in Europe, and overextended leverage positions. While short-term corrections have pressured prices, the resilience of leading assets, particularly Bitcoin, Ethereum, and BNB, underscores the continued depth and maturity of the digital asset market even amid heightened volatility.

Weekly Return of the Top 10 Cryptocurrencies by Market Capitalization (excluding Stablecoins)

Source: TradingView.com (As of November 9, 2025)

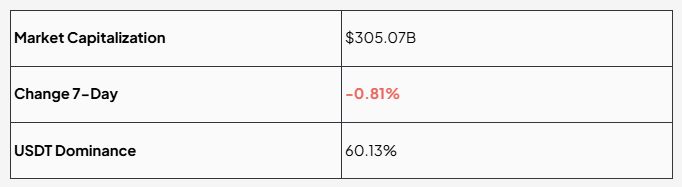

Stablecoins

The stablecoin market remained relatively steady this week, with total capitalization at $305.07 billion, marking a modest 0.8% decline over the past seven days. Despite the slight pullback, stablecoins continue to anchor liquidity in the crypto ecosystem as investors adopted a more cautious stance amid risk-off sentiment.

Tether (USDT) retained its dominance, representing 60.1% of the market with a supply above $183 billion, reaffirming its role as the primary liquidity driver. Ethereum led network activity, holding 54.8% of stablecoin market share with $167.18 billion in capitalization, up 1.2% on the week. This reflects steady on-chain liquidity and DeFi demand. Tron followed with 25.6% ($78.03 billion, down 0.6%), while Solana saw a sharper 5.2% decline to $13.84 billion, mirroring weakness across Solana-linked assets.

Overall, the mild contraction in capitalization aligns with broader market caution following renewed concerns about delayed U.S. rate cuts and tighter European regulation. Still, elevated USDT dominance, Ethereum's expanding stablecoin base, and strong DEX activity continue to highlight the sector's resilience and its essential role as the backbone of digital asset liquidity.

Key Metrics

Source: DefiLlama.com (As of November 9, 2025)

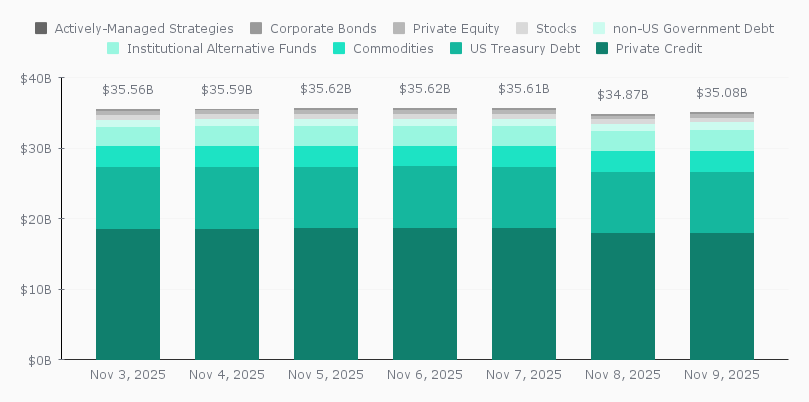

Tokenized Real-World Assets (RWA)

The Real-World Asset (RWA) market posted a 1.3% increase this week, bringing total value to $35.08 trillion. The steady rise reflects broad-based stability across major segments, supported by renewed inflows into alternative and sovereign products. Growing institutional interest in tokenized instruments, particularly after new infrastructure initiatives and clearer regulatory frameworks in major markets, has helped reinforce investor confidence.

Private Credit remained the dominant component, holding near $18.6 trillion and representing over half of total RWA value. U.S. Treasury Debt saw a mild uptick to $8.69 trillion, highlighting sustained demand for tokenized government securities as investors continue to favor lower-risk yield exposure.

Among other categories, Commodities advanced slightly to $2.96 trillion, reflecting stronger activity in tokenized gold and metals products, while Institutional Alternative Funds climbed to $2.98 trillion, signaling renewed institutional participation in structured and real-estate-backed RWAs. Non-U.S. Government Debt edged higher to $1.04 trillion, suggesting moderate diversification into international sovereign assets.

Smaller segments, including Private Equity ($521 billion), Corporate Bonds ($259 billion), and Actively Managed Strategies ($315 million), remained stable, with consistent engagement but limited new inflows.

Overall, the week's modest growth underscores continued institutional adoption and infrastructure expansion in tokenized real-world instruments, confirming RWAs' position as a cornerstone of the digital asset market.

Total Tokenized Real-Word Assets Onchain

Source: RWA.xyz (As of November 9, 2025)

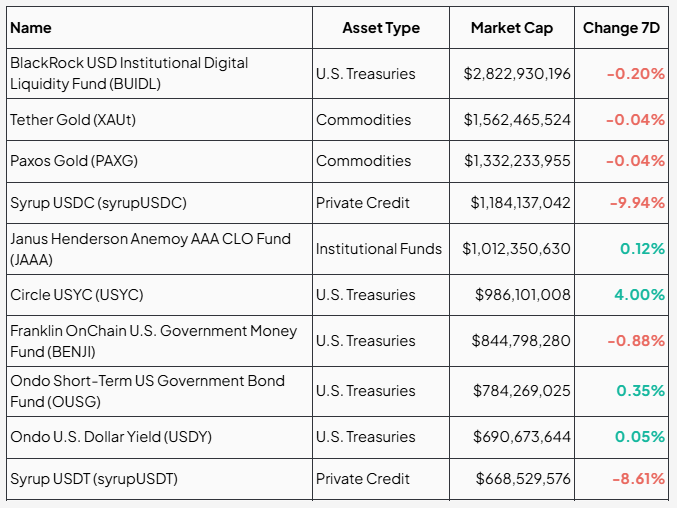

Top Ten Tokenized RWA

The leading tokenized RWA products reflected mixed performance this week, with most U.S. Treasury-backed funds showing moderate growth, while private credit vehicles and commodity-linked tokens experienced minor declines. The overall trend points to a steady demand for tokenized sovereign exposure amid cautious risk sentiment.

BlackRock's USD Institutional Digital Liquidity Fund (BUIDL) remained the largest RWA product, with a market cap of $2.82 billion, dipping slightly by 0.2%. The fund continues to anchor the tokenized Treasuries segment, serving as a benchmark for institutional-grade digital liquidity. Other Treasury-backed funds performed well, Circle's USYC rose 4.0% to $986 million, while Ondo's OUSG and USDY posted smaller gains of 0.35% and 0.05%, respectively, highlighting consistent investor preference for on-chain short-term government debt.

In contrast, Franklin Templeton's BENJI fund slipped 0.88% to $845 million, suggesting mild outflows likely tied to profit-taking or rebalancing after recent inflows.

Commodity-backed RWAs were broadly stable: Tether Gold (XAUt) and Paxos Gold (PAXG) both edged down 0.04%, maintaining strong market caps above $1.3 billion, supported by continued interest in tokenized precious metals as an inflation hedge.

The private credit segment was weaker, with Syrup USDC and Syrup USDT down 9.9% and 8.6%, respectively, indicating reduced lending activity or capital rotation into more liquid assets.

Meanwhile, institutional allocations remained firm, Janus Henderson's Anemoy AAA CLO Fund (JAAA) rose 0.12% to $1.01 billion, reflecting growing confidence in tokenized structured credit products.

Overall, this week's data underscores a two-speed market: investors continue to favor tokenized Treasuries and institutional-grade credit, while private credit RWAs faced short-term adjustments as liquidity concentrated in lower-risk, yield-generating instruments.

Source: RWA.xyz (As of November 9, 2025)

Macroeconomic Factors

Key Takeaways

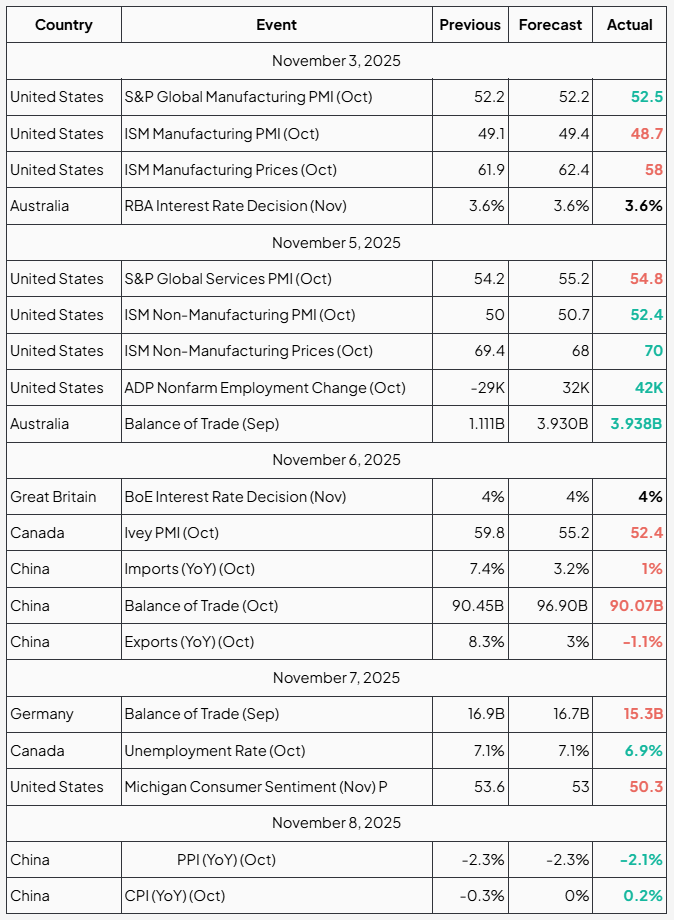

U.S. manufacturing activity contracts again in October

The ISM Manufacturing PMI fell to 48.7% in October, down from 49.1% in September, marking the eighth consecutive month of contraction in U.S. factory activity. Readings below 50 indicate a decline in overall manufacturing conditions, reflecting weak demand and slowing production. Key components of the index, including new orders (49.4%), production (48.2%), and employment (46.0%), remained in contraction territory, signaling continued softness in the sector. Meanwhile, the prices index rose to 58%, suggesting that inflationary pressures persist despite the broader slowdown. The data underscore a challenging environment for manufacturers amid cautious business spending and lingering cost pressures, even as the wider U.S. economy shows signs of resilience in services and consumer activity.

In contrast, the S&P Global U.S. Manufacturing PMI painted a slightly more positive picture, rising to 52.2 in October from 52.0 in September, indicating a modest expansion in manufacturing activity. The S&P survey reported the strongest increase in new orders in nearly two years, hinting at improving demand conditions. However, employment growth slowed, and inventories grew only marginally, suggesting that manufacturers remain cautious despite early signs of recovery.

The divergence between the ISM and S&P readings highlights the mixed signals in the U.S. industrial landscape, with one index showing ongoing contraction and the other reflecting a tentative rebound, underscoring an uneven path toward stabilization in the manufacturing sector.

RBA holds interest rate steady at 3.6% amid persistent inflation pressures

The Reserve Bank of Australia (RBA) has decided to maintain its benchmark cash rate at 3.6% during its November 2025 policy meeting, extending its pause on monetary tightening for a fourth consecutive month.

In its statement, the RBA said the decision reflects a balance between slowing economic growth and stubbornly high inflation, which remains above the Bank's 2-3% target range. Governor Michele Bullock noted that while wage growth and employment remain strong, household spending is softening, and global financial conditions continue to weigh on economic activity.

The RBA emphasized that it remains vigilant about inflation risks, particularly in services and housing, but signaled no immediate need for further rate hikes unless inflationary pressures re-accelerate. Analysts say the central bank is likely to hold rates at this level into early 2026 before considering gradual cuts if inflation shows sustained improvement.

For homeowners and businesses, the decision provides short-term stability in borrowing costs but maintains financial pressure amid elevated mortgage and credit rates.

U.S. services sector expands in October but inflation pressures remain elevated

The U.S. services economy continued to grow in October, though signs of cost pressure and slower momentum emerged across key indicators.

The S&P Global Services PMI rose to 54.8, up from 54.2 in September, marking one of the strongest readings of 2025 and signaling steady demand across business and consumer services. Similarly, the ISM Non-Manufacturing PMI increased to 52.4 from 50.0, showing that activity remains in expansion territory for a second consecutive month.

However, the ISM Non-Manufacturing Prices Index climbed to 70, up from 69.4, highlighting persistent input cost inflation despite moderating wage pressures. Survey respondents cited higher energy and logistics costs as key contributors to the increase.

Economists note that the data reinforce a picture of resilient U.S. service-sector growth, even as inflation risks linger. The combination of steady output and strong prices may complicate the Federal Reserve's path toward monetary easing, as policymakers weigh how quickly inflation can return to target without stalling growth.

U.S. private sector adds 42,000 jobs in October, signaling modest labor market recovery

The ADP National Employment Report showed that the U.S. private sector added 42,000 jobs in October, marking a return to positive territory after a revised decline of 29,000 in September. The figure came in slightly above expectations of around 32,000, suggesting that hiring momentum is stabilizing after two months of weakness.

ADP's data showed that job creation was led by the services sector, particularly in health care, education, and leisure and hospitality, while manufacturing and construction employment remained largely flat. Wage growth continued to slow, rising just 4.7% year-over-year, the smallest increase since mid-2021 , a sign that labor cost pressures may be easing.

ADP Chief Economist Nela Richardson said the report "shows a cooling but resilient labor market," noting that employers remain cautious about expanding headcount amid economic uncertainty and tighter financial conditions.

The results align with expectations for the upcoming official U.S. nonfarm payrolls report, which economists anticipate will also reflect moderate job gains and softening wage growth, consistent with a gradual rebalancing of the post-pandemic labor market.

Bank of England holds interest rate at 4% amid divided committee and easing inflation

The Bank of England (BoE) voted to maintain its benchmark interest rate at 4% during its November 2025 policy meeting, pausing its recent cycle of rate cuts as inflation shows early signs of moderating.

The decision was narrowly split, with five members of the Monetary Policy Committee (MPC) voting to hold rates and four favoring a 25-basis-point cut to 3.75%. The Bank cited the need for more evidence that inflation is sustainably moving toward its 2% target before further easing monetary policy.

Governor Andrew Bailey noted that while headline inflation has fallen to around 3.8%, it remains elevated, and services inflation continues to show persistence. "We need to be sure the progress we've made isn't reversed," Bailey said, emphasizing a cautious approach to policy adjustments.

Markets had largely anticipated the hold decision, with investors now expecting a potential rate cut in December or early 2026 if economic data confirm a slowdown in wage growth and consumer prices.

The BoE's stance reflects a broader global trend among central banks, including the Federal Reserve and the European Central Bank, which are opting for extended pauses as they balance cooling inflation against risks of weakening growth.

U.S. consumer sentiment plunges to 50.3 in November amid government shutdown concerns

The University of Michigan's preliminary Consumer Sentiment Index fell sharply to 50.3 in November, down from 53.6 in October and well below market expectations of 53. The reading marks the lowest level of consumer confidence since mid-2022, signaling growing pessimism about the economic outlook.

Survey director Joanne Hsu reported that sentiment weakened across all income and demographic groups, with notable declines in assessments of both personal finances and broader business conditions. The index's Current Conditions component dropped to 52.3 from 58.6, while Consumer Expectations slipped to 49.

The decline was largely attributed to anxiety surrounding the ongoing U.S. government shutdown, uncertainty over fiscal negotiations, and lingering concerns about inflation and interest rates. Short-term inflation expectations edged higher to 4.7%, while long-term expectations remained steady at 3.6%, reflecting continued caution among consumers.

Economists warn that the downturn in sentiment could weigh on household spending, which accounts for roughly two-thirds of U.S. GDP. If sustained, this weakness may complicate the Federal Reserve's path toward achieving a "soft landing" while managing inflation risks.

China's exports fall 1.1% in October as global demand cools and trade surplus narrows

China's latest trade data for October 2025 showed renewed weakness in the country's export engine, underscoring challenges to both external and domestic demand.

Exports fell 1.1% year-over-year, reversing September's strong 8.3% gain and marking the first monthly decline in five months. The drop was driven largely by a 25% plunge in shipments to the United States, reflecting continued global demand softness and the lingering impact of trade tensions.

Imports grew just 1%, down sharply from 7.4% in September, signaling fragile domestic consumption and limited appetite for raw materials amid an ongoing property market slump. As a result, China's trade surplus narrowed to $90.07 billion, below expectations of around $96.9 billion.

Economists note that the data highlight China's uneven post-pandemic recovery. While manufacturing activity has shown some stabilization, external demand remains subdued and domestic stimulus measures have yet to translate into stronger import growth.

Analysts expect the People's Bank of China (PBoC) to maintain an accommodative stance and potentially deliver targeted stimulus to support exporters and bolster domestic confidence. The weaker trade figures also reinforce expectations that Beijing may increase fiscal spending to meet its 2025 growth targets.

China's consumer prices rise 0.2% in October, signaling tentative recovery from deflation

China's Consumer Price Index (CPI) rose by 0.2% year-over-year in October, ending a three-month streak of declines and offering cautious optimism that the world's second-largest economy is emerging from deflationary territory. The reading slightly exceeded market expectations for flat growth and followed a 0.3% decline in September.

The data showed that core inflation, which excludes volatile food and energy prices, climbed to 1.2%, its highest level in nearly two years, suggesting a gradual pickup in underlying demand. However, food prices fell 2.9%, highlighting continued weakness in household consumption and retail activity.

At the same time, the Producer Price Index (PPI) fell 2.1% year-over-year, marking the 18th consecutive month of factory-gate deflation. This indicates that while consumer prices are stabilizing, input costs and manufacturing margins remain under pressure.

Economists say the modest CPI rebound reflects early effects of government stimulus and seasonal spending but warn that deflation risks have not fully disappeared. Analysts expect the People's Bank of China (PBoC) to maintain a supportive stance, potentially introducing targeted monetary easing to reinforce domestic demand and business confidence.

Canada's unemployment rate falls to 6.9% in October as job gains surpass expectations

Canada's unemployment rate declined to 6.9% in October, down from 7.1% in September and below economists' forecasts for no change, signaling a stronger-than-expected rebound in the labor market.

According to Statistics Canada, the economy added roughly 66,600 new jobs, reversing prior losses and marking the strongest employment gain since early summer. The improvement was driven by private-sector hiring, particularly in wholesale and retail trade, transportation, and information and recreation services.

However, the report also highlighted some imbalances: most of the gains were in part-time positions, while full-time employment declined by 18,500, suggesting that underlying labor demand remains uneven. The goods-producing sectors, including construction and manufacturing, continued to shed jobs, reflecting broader industrial weakness.

Economists said the surprise strength in hiring could prompt the Bank of Canada to delay additional rate cuts, as policymakers assess whether labor market resilience risks reigniting inflation pressures. The Canadian dollar strengthened modestly following the release, while government bond yields rose as traders trimmed expectations for near-term easing.

Week's Overview

Source: Investing.com

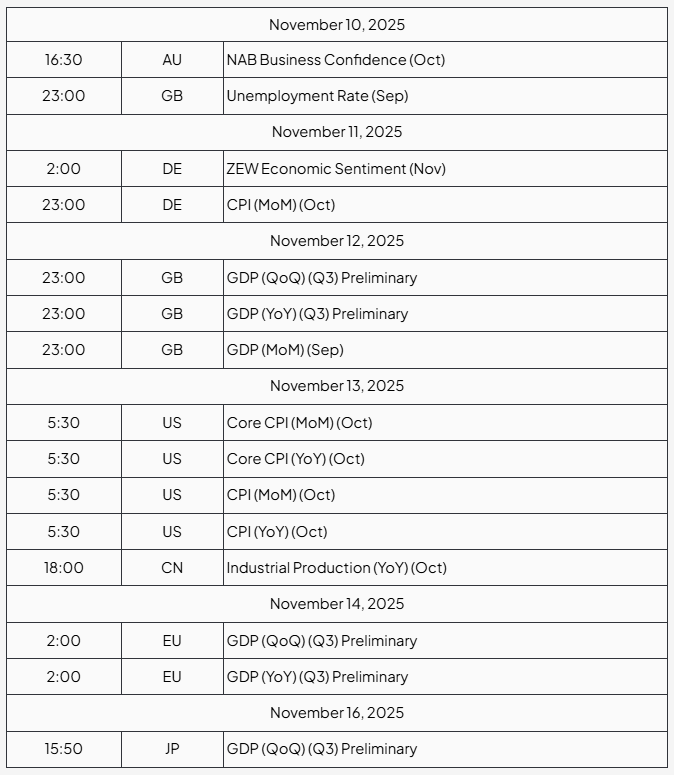

The Week Ahead

Next week, market attention will focus on inflation data from Germany and the U.S. , which will provide fresh signals about price trends and potential monetary policy decisions. Growth figures from the United Kingdom and Japan will also be closely watched, offering key insights into the pace and resilience of their economies.

Source: Investing.com Time: (GMT/UTC - 8h)

Regulation Environment

Ripple enters U.S. market with digital-asset spot prime brokerage

Ripple has officially launched its digital-asset spot prime brokerage services in the United States, marking a major expansion of its institutional offerings. The new service, enabled through Ripple's recent acquisition of Hidden Road, now rebranded as Ripple Prime, provides institutional clients with over-the-counter (OTC) spot trading, financing, and clearing for major digital assets including XRP and the stablecoin RLUSD. This move strengthens Ripple's push to bridge traditional finance and the crypto ecosystem, offering secure, compliant, and liquidity-focused access to digital markets. The company's U.S. debut of Ripple Prime underscores its evolution from a blockchain payments provider into a comprehensive institutional financial infrastructure firm

Kraken enables crypto collateral for EU derivatives trading

Kraken has introduced a new feature allowing European traders to post cryptocurrencies as collateral on its MiFID II-regulated derivatives platform. Operated through its Cyprus-based entity, Payward Europe Digital Solutions (CY) Ltd, the platform lets clients in the European Economic Area trade perpetual and fixed-maturity futures contracts while using assets like Bitcoin and Ethereum directly as collateral. This move enhances capital efficiency and trading flexibility, eliminating the need to convert crypto holdings into fiat before participating in derivatives markets. By integrating this functionality within a fully MiFID-regulated framework, Kraken strengthens its compliance posture and broadens access to sophisticated trading tools for both retail and institutional investors across the EU.

France moves to tax large crypto holdings as "unproductive wealth"

French lawmakers have approved a new measure that would classify large cryptocurrency holdings as "unproductive wealth", subjecting them to a 1% annual tax if total idle assets exceed €2 million. The proposal, passed by France's lower house on October 31, 2025, expands the nation's wealth-tax framework to include digital assets alongside gold, art, and other non-income-generating assets. The goal is to encourage investors to channel their wealth into productive sectors such as business and innovation rather than passive holdings. While the measure has not yet completed the full legislative process, it signals France's intent to bring cryptocurrency wealth into mainstream fiscal policy, a move that could reshape how digital assets are held and reported by affluent investors.

India´s Madras High Court legally recognized XRP as property, granting it protection under criminal law.

Strategy launches STRE, its first Euro-denominated perpetual preferred stock offering 3.5M shares at 100 euro each with 10% annual dividends, with proceeds going toward Bitcoin acquisition.

Madras High Court declares XRP as legal property in landmark Indian ruling

In a groundbreaking judgment this week, the Madras High Court of India ruled that cryptocurrencies like XRP are legally considered property, not merely digital tokens or speculative assets. The case stemmed from a dispute involving Indian crypto exchange WazirX, which attempted to offset losses from its $235 million hack by reallocating user-held XRP.

The court blocked WazirX's move and affirmed that virtual assets such as XRP are "intangible property capable of being held in trust, possessed, and enjoyed beneficially" under Indian law. This marks the first time an Indian court has explicitly recognized crypto as property.

Legal experts say the decision strengthens investor protection and exchange accountability, setting a precedent that digital assets fall under property rights rather than unregulated digital goods. Although the ruling applies to one specific case, it could influence future regulation and judicial interpretation of cryptocurrencies across India.

Europe narrowly avoids mass message scanning as Germany blocks "Chat Control" proposal

The European Union has narrowly avoided passing the controversial "Chat Control" regulation, which would have required messaging platforms to scan private communications for illegal content, including encrypted chats. The bill, formally known as the Regulation to Prevent and Combat Child Sexual Abuse (CSAR), stalled this week after Germany refused to back it, preventing the formation of a qualified majority in the EU Council.

Germany's Justice Minister, Marco Buschmann, said mass surveillance of private messages "must be taboo in a constitutional state," arguing that the proposal violated privacy rights and undermined end-to-end encryption. Other member states, including Austria and the Netherlands, voiced similar concerns.

Privacy advocates across Europe hailed the outcome as a temporary victory for digital rights, though warned that the legislation could return in a revised form. Critics say the proposal's broad scanning mandates would have created infrastructure for mass surveillance by default, fundamentally eroding online privacy.

Observers also note that without privacy-preserving architecture at the protocol level, Web3 and decentralized networks could replicate the same surveillance chokepoints that this proposal sought to formalize. The debate, they argue, underscores the importance of designing privacy by default into next-generation internet systems.

Franklin Templeton launches tokenized USD money market fund in Hong Kong

Global investment firm Franklin Templeton has launched a tokenized U.S. dollar-denominated money market fund in Hong Kong, marking a major step in bringing traditional finance onto blockchain infrastructure. The new fund, called the Franklin OnChain U.S. Government Money Fund, issues each share as a digital token recorded on a public blockchain, providing greater transparency and operational efficiency.

The fund invests primarily in short-term U.S. government securities, repurchase agreements, and cash, mirroring the structure of Franklin Templeton's existing U.S. on-chain money market product. It is currently available to professional and institutional investors in Hong Kong under the city's regulated framework for digital assets.

Franklin Templeton is partnering with HSBC and OSL Group to handle settlement, custody, and distribution, ensuring compliance with the Hong Kong Monetary Authority's (HKMA) Fintech 2030 strategy, which promotes tokenization of real-world assets (RWAs).

The firm said it plans to seek regulatory approval for a retail version of the fund in the near future. The launch positions Hong Kong as a regional leader in regulated tokenized finance, following similar initiatives by the HKMA and the city's push to attract global asset tokenization projects.

Industry analysts see the move as a milestone in institutional adoption, demonstrating how blockchain technology can modernize fund management and global liquidity without compromising compliance or investor protection.

Technology and Innovation

Fireblocks, Solana, TON, Polygon, and Stellar launch Blockchain Payments Consortium to unify crypto standards

A coalition of leading blockchain and infrastructure projects, including Fireblocks, Solana Foundation, TON Foundation, Polygon Labs, and the Stellar Development Foundation, has announced the creation of the Blockchain Payments Consortium (BPC). The initiative aims to establish unified standards for crypto payments, focusing on interoperability, compliance, and stablecoin transaction frameworks.

The consortium seeks to address one of the industry's biggest challenges: fragmented payment systems across blockchains. By developing shared technical and regulatory standards, the group intends to make digital asset payments faster, more secure, and more compatible with traditional financial systems.

Fireblocks CEO Ran Goldi described the initiative as "a milestone toward making blockchain payments as seamless as card transactions," while TON Foundation's Nikola Plecas emphasized that collaboration among major networks "is essential to scale global crypto payments responsibly."

This alliance marks a new phase in blockchain development, signaling a shift from competition to cooperation and standardization. Analysts see the BPC as a potential game-changer for stablecoin adoption, cross-chain settlements, and enterprise-grade payment infrastructure.

Tangem launches Tangem Pay to let users spend USDC via Visa virtual card

Hardware wallet maker Tangem has unveiled Tangem Pay, a new payment feature that enables users to spend USDC directly from their self-custodial wallets using a Visa virtual card.

Tangem Pay links users' on-chain balances to a Visa payment account, allowing them to make purchases wherever Visa is accepted. Funds remain in the user's control until the moment of payment, when the equivalent amount of USDC is converted 1:1 to fiat currency and settled through Visa's network.

The service initially supports USDC on the Polygon network, with plans to integrate additional stablecoins and blockchains in future updates. Tangem confirmed that KYC verification is required to activate Tangem Pay accounts, although the standard Tangem Wallet remains fully self-custodial and does not require identity verification.

Tangem Pay will roll out gradually across regions - starting with the U.S., Latin America, and parts of Asia-Pacific, followed by the UK and EU in early 2026. The company emphasized that the service carries no monthly or transaction fees, apart from blockchain network and Visa foreign-exchange costs.

Industry analysts view Tangem Pay as a significant bridge between on-chain stablecoin assets and traditional payment systems, marking another step toward everyday crypto-based payments.

Google integrates Polymarket and Kalshi data into search results, bringing crypto prediction markets into the mainstream

Google has begun displaying live prediction market data from Polymarket and Kalshi directly in its search results and Google Finance platform, marking a new step in blending traditional and crypto-based financial data.

The update allows users to view real-time probabilities for major political, economic, and social events, such as elections, inflation forecasts, or sports outcomes, simply by searching related questions. The data sources come from both Kalshi, a CFTC-regulated U.S. prediction exchange, and Polymarket, a decentralized blockchain-based platform built on Polygon, where users trade outcomes using USDC.

While Kalshi represents traditional, regulated markets, Polymarket introduces on-chain data to Google's ecosystem, highlighting the growing influence of crypto-native prediction markets. Industry analysts view this integration as a sign that blockchain-based market data is being normalized within mainstream financial tools, potentially paving the way for deeper use of decentralized feeds in global finance.

RedStone launches Credora to bring dynamic risk ratings to DeFi lending

Data oracle provider RedStone has launched Credora, a new platform designed to deliver real-time, dynamic risk ratings for decentralized finance (DeFi) lending protocols. The system provides continuously updated insights into protocol health, default probabilities, and liquidity conditions, aiming to make DeFi lending more transparent and institution-friendly.

Unlike traditional rating models that rely on static, periodic assessments, Credora uses on-chain data, market volatility signals, and liquidity metrics to generate dynamic risk scores. These metrics can be integrated directly into lending platforms through APIs, helping protocols and institutional investors monitor exposure and adjust collateral or rates accordingly.

Credora's initial integrations include Morpho and SparkLend, two leading DeFi lending protocols. The launch follows the recent $20 billion liquidation wave in October, underscoring the need for stronger risk management tools in decentralized markets.

According to RedStone, Credora aims to bridge the gap between DeFi's open infrastructure and traditional financial risk standards, setting a new benchmark for how on-chain creditworthiness can be measured and acted upon. Analysts view this as a critical step toward safer, data-driven DeFi lending ecosystems.

Ethereum protocols launch EPAA to give on-chain infrastructure a voice in policymaking

Seven leading protocols in the Ethereum ecosystem, namely Aave Labs, Aragon, Curve Finance, Lido Labs Foundation, Spark Foundation, The Graph Foundation and Uniswap Foundation, announced the creation of the Ethereum Protocol Advocacy Alliance (EPAA). The alliance aims to ensure that the builders and operators of on-chain infrastructure have direct input into the shaping of regulatory and policy frameworks.

With over $100 billion in non-custodial assets secured across their protocols, the founding members say this step is designed to balance the current influence of centralized crypto players in policymaking. The EPAA's priorities include protecting protocol neutrality, promoting real-time on-chain transparency, preserving innovation flexibility, and maintaining global permissionless access. The group will coordinate with existing advocacy organisations rather than operate as a typical lobbying entity.

By integrating technical insight from core infrastructure teams directly into policy discussions, the EPAA hopes to ensure that regulation properly reflects how decentralised systems operate, instead of forcing them into outdated centralized models.

Standard Disclaimer: This report is provided for informational purposes only and does not constitute legal, financial, or investment advice. The views expressed represent the author's perspective at the time of publication and may change as market conditions develop. Although the information is drawn from sources deemed reliable, its accuracy and completeness are not guaranteed. Readers should exercise their own judgment and perform due diligence before making any decisions based on this report.

Contributors

Ana CabaleiroFinancial Analyst