Research

Weekly Market Recap - November 16, 2025

Global markets traded defensively this week as equity gains narrowed, commodities softened, and the dollar strengthened, while crypto markets and tokenized RWAs declined amid de-risking flows, rising volatility, and cautious sentiment driven by uneven macro data and regulatory reactivation.

Download the PDF

Estimated Reading Time: 19 minutes

Summary

Last week was marked by mixed market performance, a clear turn toward risk aversion, and continued development in digital-asset regulation and infrastructure. In traditional markets, U.S. equities hovered near record levels but showed little momentum, with gains concentrated in a narrow group of large-cap names. The Nasdaq slipped while the Dow and S&P 500 were mostly flat, underscoring weak breadth. Commodities softened, oil fell below $60 and gold pulled back, while the U.S. dollar strengthened against major currencies. Treasury yields were broadly stable as markets awaited clearer macro signals. Global economic data painted an uneven picture: the U.K. labor market cooled sharply, Germany's sentiment weakened, EU growth remained sluggish, China's industrial activity slowed, Japan contracted in Q3, and Australia showed a temporary rebound in employment.

Crypto markets and tokenized real-world assets (RWA) both reflected a more defensive tone. Total crypto market capitalization fell 5.7%, driven by steady selling and a mid-week surge in trading volumes that pointed to active de-risking. Major assets like Bitcoin, Ethereum and Solana declined, while stablecoins held firm at around $304B and slightly increased their market share as capital moved toward safety. In parallel, total on-chain RWA value fell nearly 4%, led by a more than 7% contraction in private credit and declines in tokenized equities and private equity. Yet some segments showed resilience, with non-U.S. government debt expanding sharply and commodity-backed tokens such as XAUt and PAXG posting modest gains. Among top RWA products, BlackRock's BUIDL saw a notable 10.6% outflow, whereas U.S. Treasury-linked funds like USYC and WTGXX recorded strong weekly inflows. Private-credit tokens Syrup USDC and Syrup USDT also grew, illustrating selective rotation rather than broad retreat across digital assets.

The end of the U.S. government shutdown has reopened key regulatory processes, clearing backlogs at agencies like the SEC and CFTC and setting the stage for faster decisions on crypto ETFs and policy. Globally, Brazil finalized its first comprehensive crypto framework, while real-world assets expanded on Solana through Figure's YLDS launch. U.S. market activity accelerated with 21Shares debuting the first 1940-Act crypto index ETFs, SoFi becoming the first chartered bank to offer direct in-app crypto purchases, and Canary Capital launching the first spot XRP ETF. Transak broadened its U.S. licensing footprint, the IRS reaffirmed crypto-as-property tax treatment with updated gift thresholds, and a new Senate draft bill proposes expanding CFTC oversight to bring more structure and clarity to U.S. digital-asset regulation.

Platform innovation remained strong despite market softness: OKX broadened access to Solana-ecosystem tokens on its DEX; Coinbase re-entered primary launches with a new token-sale platform; Cash App announced support for Solana-based USDC payments for early 2026; and Visa launched a pilot enabling fiat-funded payouts that recipients can receive in stablecoins. These developments signal ongoing progress toward faster payments, multi-chain interoperability, and deeper integration of blockchain rails into mainstream financial products.

Market Confidence and Adoption

Broad Markets

Global markets delivered a mixed performance this week as investors navigated uneven sector trends, shifting risk sentiment, and diverging moves across major asset classes. U.S. equities remained close to record highs, but trading was choppy as market leadership stayed concentrated in a narrow group of large-cap names.

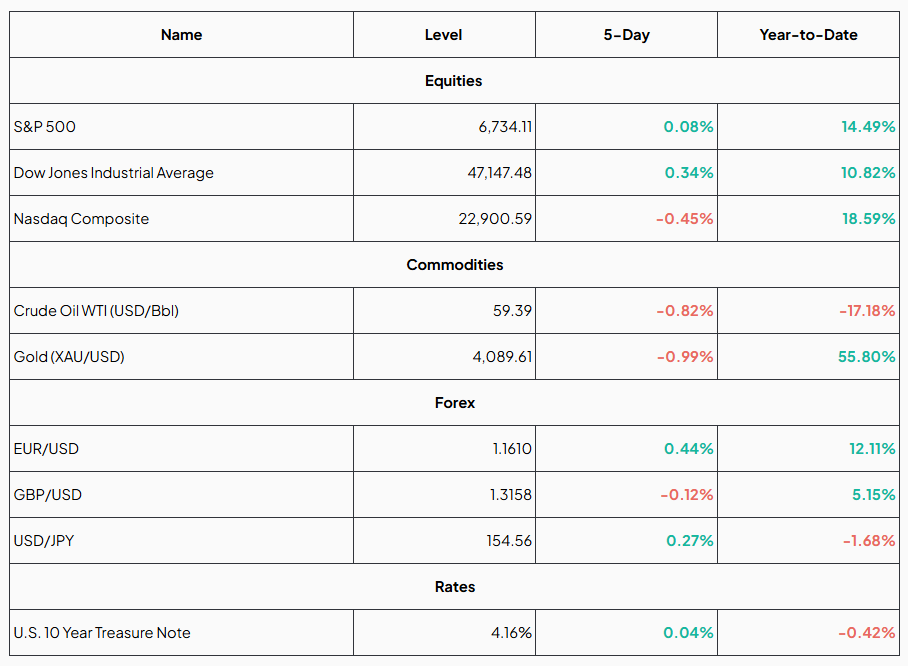

U.S. equity indexes showed limited momentum. The S&P 500 inched up 0.08% over the past five days, while the Dow Jones Industrial Average rose a modest 0.34%, supported by strength in a handful of defensive and industrial components. In contrast, the Nasdaq Composite slipped 0.45%, reflecting pressure on high-growth and technology shares after their strong gains. Analysts continue to caution that most of the market's progress has come from a small cluster of mega-cap leaders, heightening worries about breadth and the durability of the rally.

Commodity markets also painted a cautious picture. Crude oil (WTI) extended its decline, falling 0.82% on the week. Persistent concerns about global demand, particularly in Asia, alongside steady production levels kept prices below the $60 threshold. Meanwhile, gold pulled back nearly 1% on the week. The slight decline suggests some consolidation after significant safe-haven inflows, even as geopolitical tensions and macro uncertainty remain elevated.

In foreign exchange, the U.S. dollar regained strength, supported by uneven global growth signals and investors' preference for safety. The euro climbed 0.44% over the week but remains overshadowed by broader dollar resilience, while the pound slipped 0.12% as mixed economic data weighed on sentiment. The Japanese yen weakened slightly, with USD/JPY rising 0.27%, though its performance indicates modest stabilization as U.S. yields edge lower from earlier highs.

Treasury markets were calm, with the U.S. 10-Year Treasury yield ticking higher by just 0.04 percentage points to 4.16%. The modest move reflects a market in wait-and-see mode. Investors continue to balance signs of cooling inflation against uncertainty surrounding the Federal Reserve's policy path. The relatively steady yield environment underscores a cautious outlook, as traders look for clearer direction from upcoming economic releases and central bank communications.

Weekly Market Data

Source: MarketWatch.com , Google Finance, TradingView (As of November 16, 2025)

Cryptocurrencies

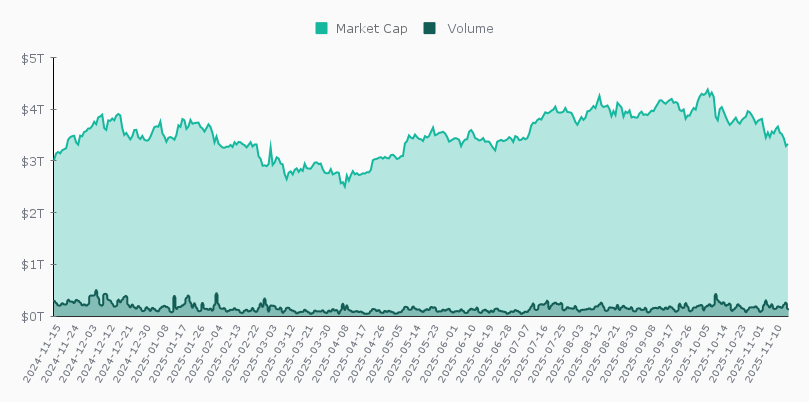

The cryptocurrency market experienced a week of heightened volatility, with total market capitalization and trading volumes shifting notably as participants adjusted their positions in response to changing sentiment and a softer risk environment. After a period of sustained strength, momentum faded, resulting in a 5.72% decline in total market cap for the week.

The pullback unfolded gradually, with market cap trending lower across several consecutive sessions. Mid-week, trading activity spiked, indicating that the downturn was driven more by active repositioning than by a slow, passive drift. The surge in volume during the selloff suggested that traders were reacting to short-term pressures, accelerating the decline and contributing to widespread weakness across major tokens.

Toward the end of the week, conditions stabilized somewhat, with volumes easing and price action becoming less abrupt. However, this stabilization resembled a pause rather than the start of a meaningful recovery. The rebound lacked follow-through, underscoring a market still searching for direction.

Overall, the week's developments highlight a digital-asset landscape under noticeable pressure. Valuations retreated, bursts of elevated trading activity marked periods of intensified selling, and the late-week calm did little to shift sentiment. Market participants remain cautious, waiting for clearer macro signals and stronger conviction before re-engaging more aggressively. In the absence of a compelling catalyst, the market appears to be entering a consolidation phase, awaiting its next driver.

Crypto Market Capitalization and Volume

Source: CoinGecko.com

Following the broader market pullback described above, individual asset performance reflected the same cautious tone. Across major cryptocurrencies, weekly movements showed widespread declines in market capitalization, accompanied by modest shifts in market share as capital rotated toward perceived safety.

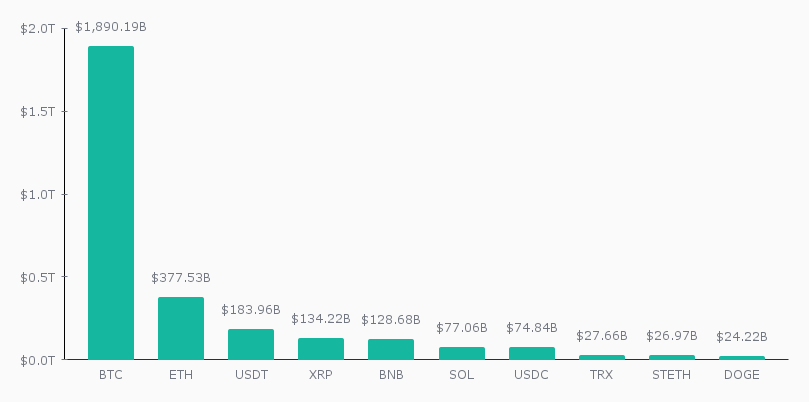

Bitcoin, which continues to lead the market, fell from $2.08 trillion to $1.89 trillion, though its dominance held steady, with market share edging only from 57.6% to 57.2%. This indicates that the selloff was broad-based rather than concentrated in Bitcoin specifically.

Ethereum mirrored this broader weakness. Its market cap dropped from $431 billion to $377 billion, with market share slipping from 11.9% to 11.4%, reflecting a slightly sharper decline than Bitcoin and underscoring softer appetite for major altcoins.

Stablecoins showed a different pattern. Tether saw a modest rise in market share, from 5.1% to 5.6%, supported by slight gains in its market cap-typical behavior in risk-off environments as traders shift toward stability. USDC also held steady, registering a mild improvement in its share of the market.

Most other major altcoins experienced declines. XRP, BNB, Solana, Dogecoin, and Lido Staked Ether all posted lower market caps versus the prior week. Solana was among the most impacted, falling from $91.6 billion to $77 billion, with its market share dipping from 2.5% to 2.3%, highlighting heavier pressure on higher-beta assets. TRON was one of the few exceptions, staying nearly unchanged at around $27.6 billion and maintaining a stable 0.8-0.9% share.

In broad terms, the data points to a clear decrease in risk appetite: most cryptocurrencies lost value, stablecoins gained relative strength, and Bitcoin's dominance remained intact despite the overall contraction in market capitalization.

Cryptocurrency Market Share

Source: CoinGecko.com (As of November 16, 2025)

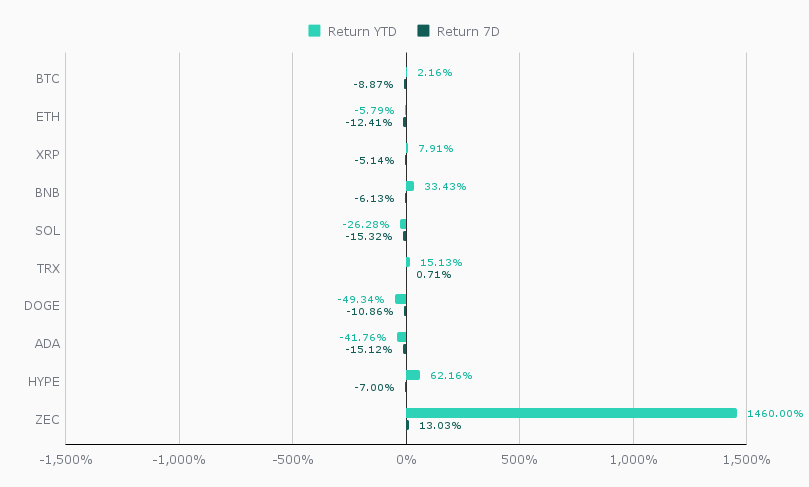

The same risk-off tone was reflected in weekly price performance. Bitcoin led the market lower with an 8.87% decline to $95,358, though it still holds a modest 2.16% gain year-to-date. Ethereum underperformed even more sharply, dropping 12.41% to $3,138 and extending its year-to-date losses to -5.79%, reinforcing ongoing softness among large-cap altcoins.

Several other major tokens followed similar patterns. BNB fell 6.13%, though its 33.43% year-to-date rise highlights its earlier strength. XRP declined 5.14% but remains positive for the year at 7.91%. Solana had one of the steepest weekly pullbacks at -15.32%, deepening its year-to-date decline to -26.28% in a continuation of its high volatility.

Sentiment-driven assets also struggled. Dogecoin dropped 10.86%, leaving it nearly -50% year-to-date, while Cardano fell 15.12%, extending its YTD downturn to -41.76%. These moves reflect a broader rotation away from speculative tokens during the week.

There were, however, a few isolated bright spots. TRON registered a 0.71% weekly gain and maintains healthy year-to-date growth of 15.13%, benefiting from its relatively steady fundamentals. Hyperliquid limited its losses to -7%, while still delivering an impressive 62.16% gain year-to-date.

The standout performer of the week was Zcash. Its price surged 13.03% to $702.20, contributing to an extraordinary 1,460% year-to-date rally. This dramatic outperformance stands in sharp contrast to the broader market retreat, reflecting a unique mix of strong narrative momentum, heightened trading activity, and renewed investor interest in privacy-focused assets.

In summary, the week underscored a decisive shift toward caution across the digital asset landscape. While most major cryptocurrencies experienced meaningful declines, a select few, most notably Zcash, managed to defy the trend with exceptional performance. The market now appears to be consolidating, waiting for the next catalyst to determine direction.

Weekly Return of the Top 10 Cryptocurrencies by Market Capitalization (excluding Stablecoins)

Source: TradingView.com (As of November 16, 2025)

Stablecoins

The stablecoin market showed minimal movement this week, with total market capitalization holding near $304.17 billion. The slight 0.25% decline over the past seven days indicates a relatively steady environment, especially compared with the broader volatility seen across major cryptocurrencies. This stability suggests that investors have not significantly shifted funds out of or into stablecoins, reinforcing their role as a parking place during uncertain market conditions.

Tether (USDT) strengthened its position this week, rising to 60.5% dominance as its supply remained firmly anchored over $184 billion, reinforcing its role as the market's core liquidity provider. Ethereum continued to lead stablecoin network activity with $165.14 billion in capitalization, representing 54.3% of all stablecoins despite a 1.1% weekly decline, still indicative of resilient on-chain liquidity and sustained DeFi usage. TRON followed with a solid 26.1% share, as its stablecoin market cap climbed to $79.33 billion, posting a notable 1.7% increase that highlights strong transactional demand on the network. Solana showed a more pronounced pullback, with its stablecoin market cap falling 3.5% to $13.41 billion, leaving it with a 4.4% share and reflecting broader weakness across Solana-linked assets.

Despite these mixed shifts across networks, stablecoins remained one of the most stable pockets of the market this week, offering a reliable buffer as broader crypto valuations came under pressure.

Key Metrics

Source: DefiLlama.com (As of November 16, 2025)

Tokenized Real-World Assets (RWA)

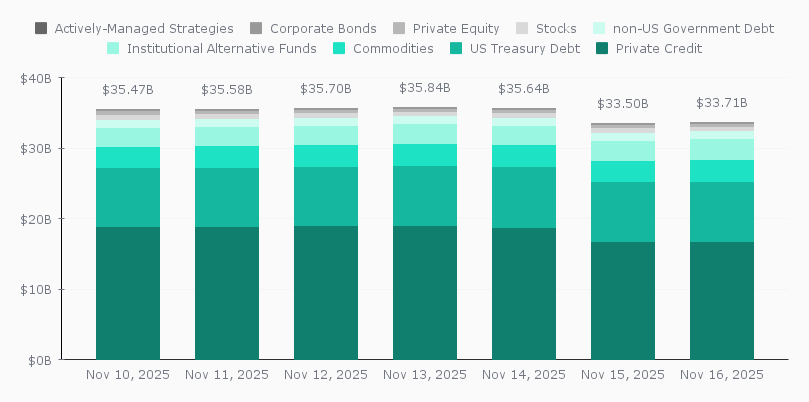

Between November 9 and November 16, 2025, the total value of tokenized real-world assets on-chain went through noticeable shifts, reflecting changes in market sentiment and investor positioning. The combined value of all tokenized assets declined by nearly 4%, marking a period of adjustment after what had been a steady expansion in previous months.

The largest category, private credit, saw a meaningful contraction of just over 7%. Its value dropped from close to 18 billion dollars to around 16.7 billion, suggesting a phase of capital outflows, asset maturities, or simple profit-taking after sustained growth. Tokenized U.S. Treasury exposure remained relatively stable, with only a small decrease, consistent with the lower volatility typically associated with government debt.

Some segments moved in the opposite direction. Tokenized commodities grew modestly, showing continued investor interest in blockchain-based representations of physical assets. The most notable expansion came from non-U.S. government debt, which increased by more than 10%. This sharp rise indicates either substantial new issuance on-chain or valuation adjustments that boosted the overall amount represented in this category.

Other areas experienced more pronounced declines. Tokenized stock exposure fell by about 4.5%, while private equity dropped nearly 15%, pointing to reduced interest in more illiquid or higher-risk segments of the market. Actively managed strategies saw the steepest fall, over 60%, which likely reflects a reallocation or reduction in the scope of strategies being tokenized rather than purely market-driven price movements. Corporate bonds, meanwhile, stayed almost flat, registering a slight increase that highlights their resilience within the tokenized fixed-income space.

In sum, the period captured a diverse set of movements across asset classes, with some categories expanding meaningfully and others contracting sharply. Together, these shifts signal a dynamic phase for the tokenized asset ecosystem, shaped by both investor sentiment and structural changes in how different types of assets are being brought on-chain.

Total Tokenized Real-Word Assets Onchain

Source: RWA.xyz (As of November 16, 2025)

Top Ten Tokenized RWA

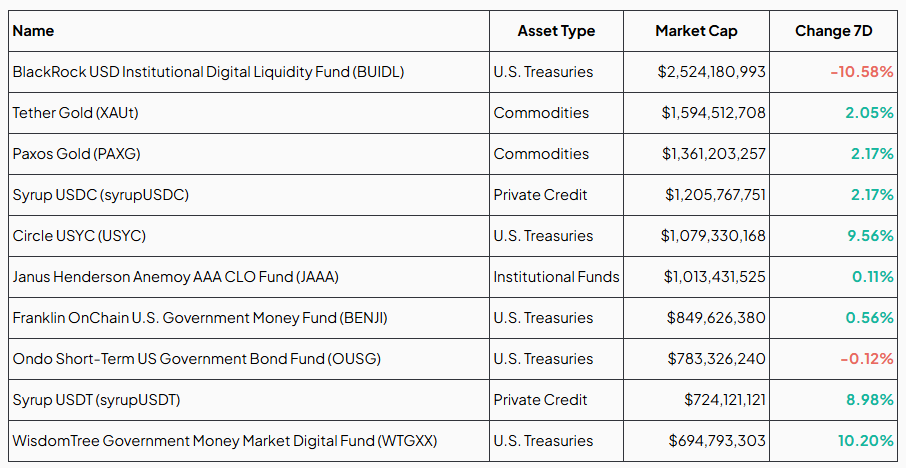

Several of the largest tokenized real-world asset products experienced notable shifts in market capitalization, reflecting both broader market dynamics and asset-specific investor flows. The BlackRock USD Institutional Digital Liquidity Fund (BUIDL), which remains the largest product in the ecosystem, saw a meaningful decline of 10.6%, bringing its market cap to approximately $2.52 billion. Despite its size and generally stable profile, this decrease suggests a significant rebalancing or short-term outflow from institutional liquidity positions.

In contrast, commodity-backed tokens demonstrated steady growth. Tether Gold (XAUt) and Paxos Gold (PAXG) both recorded weekly increases slightly above 2%, continuing the trend of rising interest in tokenized gold exposure. Their market capitalizations now stand at $1.59 billion and $1.36 billion, respectively, positioning them as two of the largest digital representations of physical commodities.

Private credit-linked tokens also showed positive momentum. Syrup USDC (syrupUSDC) grew by 2.2% to reach $1.2 billion, while Syrup USDT (syrupUSDT) rose sharply by 9%, now totaling $724 million. These increases underscore the expansion of tokenized private credit strategies, highlighting growing demand for yield-oriented assets within on-chain markets.

The U.S. Treasury-backed segment exhibited mixed performance. Circle's USYC saw a strong increase of 9.6%, pushing its market capitalization above $1.07 billion. WisdomTree's digital government money market fund (WTGXX) also recorded double-digit growth, rising 10.2% to $694 million. On the other hand, BlackRock's BUIDL declined significantly, and Ondo's OUSG experienced a slight contraction of 0.1%, suggesting varying investor behavior across different treasury-based structures. Franklin Templeton's BENJI fund maintained moderate growth at 0.6%, reaching $849 million.

Institutional alternative strategies remained stable. The Janus Henderson Anemoy AAA CLO Fund (JAAA) saw only minimal movement, rising 0.1% and maintaining a market cap near $1.01 billion. This stability reflects the relatively predictable nature of tokenized CLO exposure.

The week illustrates a diverse landscape across tokenized assets: strong gains in selected treasury and commodity products, solid growth in private credit, and a notable contraction in one major liquidity fund. These shifts highlight an increasingly dynamic market where investor preferences vary considerably across asset classes and issuers.

Source: RWA.xyz (As of November 16, 2025)

Macroeconomic Factors

Key Takeaways

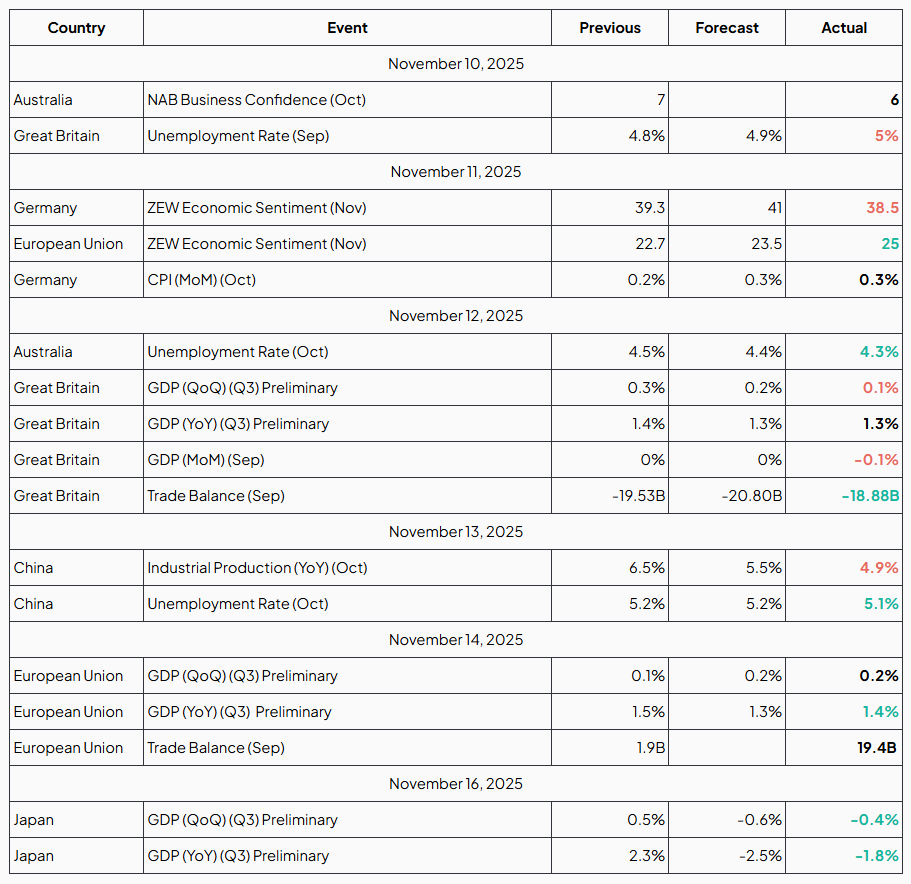

UK labour market shows clear signs of cooling

The latest data from the Office for National Statistics reveals that the UK unemployment rate climbed to 5.0% in the three months to September, up from 4.8% previously and slightly above expectations of 4.9%. This marks the highest unemployment level in roughly four years, signaling a noticeable softening in the labour market.

Alongside the rise in unemployment, wage growth continued to slow, reinforcing the picture of easing labour-market pressures. Payroll data also pointed to declining employment levels, adding to concerns about momentum in the broader economy.

For markets, the implications are clear: a cooling labour market may give the Bank of England more room to consider future rate cuts, as inflationary pressures from wages gradually ease. However, the shift also highlights growing challenges for households and businesses as economic conditions continue to soften.

German investor sentiment weakens more than expected in November

Germany's ZEW Economic Sentiment index slipped to 38.5 in November, down from 39.3 in the previous month and below market expectations of 41. The decline signals that analysts and institutional investors have grown slightly more cautious about the country's economic outlook over the next six months.

Despite a small improvement in the "Current Situation" index, overall confidence remains subdued as concerns persist about Germany's growth momentum and whether existing fiscal measures are sufficient to support a meaningful recovery. The softer reading adds to worries that Europe's largest economy may continue to face headwinds into year-end, potentially influencing broader Eurozone sentiment and policy expectations.

German inflation slows as monthly price growth eases in October

Germany's consumer inflation cooled further in October, with the CPI rising 0.2% month-on-month, coming in below both the previous reading and market expectations of 0.3%. The softer monthly figure reflects easing price pressures across key goods categories, including energy and food, while services inflation remains comparatively sticky.

On an annual basis, inflation edged down to 2.3%, reinforcing the broader trend of gradual disinflation in Europe's largest economy. Although price growth is slowing, the pace remains steady rather than sharp, suggesting the European Central Bank may continue to adopt a cautious stance as it evaluates the path of future policy decisions.

This moderation in inflation adds to signs of cooling economic momentum, offering markets additional clarity as they assess the balance between growth risks and easing price pressures heading into year-end.

Australia's unemployment rate falls as labour market strengthens in October

Australia's labour market showed renewed strength in October, with the unemployment rate easing to 4.3%, down from 4.5% in the previous month and coming in better than expectations. The improvement was driven largely by a solid rise in full-time employment, highlighting underlying resilience despite recent signs of economic softening.

The Australian Bureau of Statistics reported strong job creation, with more than 40,000 new positions added during the month, helping to reverse September's unexpected spike in unemployment. Steady participation levels and the increase in full-time roles indicate that demand for labour remains healthy.

For the Reserve Bank of Australia, the data suggests reduced urgency for near-term rate cuts, as the job market continues to hold up better than anticipated. Still, policymakers will be watching closely to assess whether this rebound signals sustained momentum or a temporary stabilisation within a cooling economic environment.

UK growth moderates in Q3 amid softer economic activity

The UK economy lost steam in the third quarter, with preliminary GDP figures showing a modest 0.1% quarter-on-quarter expansion, down from the prior quarter and slightly below consensus expectations. On an annual basis, growth slowed to 1.3%, highlighting a gradual deceleration as the year advances.

September's monthly print reinforced the softer tone, with GDP slipping 0.1%, driven largely by weaker manufacturing output. Vehicle production was a notable drag amid sector-specific disruptions. While services remained broadly stable and construction posted marginal gains, these offsets were insufficient to counter the manufacturing slowdown.

For the Bank of England, the data presents a mixed backdrop: economic momentum is clearly fading, but pockets of resilience in services suggest the downturn is not yet broad-based. The softer outlook may nonetheless influence policy discussions in the months ahead.

China's industrial output cools in October as manufacturing momentum weakens

China's industrial activity eased in October, with production rising 4.9% year-on-year, down from 6.5% in September and below market forecasts. The slowdown was widespread across manufacturing, with mining and utilities providing only modest support.

The latest figures underscore ongoing fragility in China's manufacturing base as global demand remains subdued and domestic challenges persist. Investors will now look for signs of whether this marks a temporary pause or a more sustained loss of momentum heading into the year-end. Policymakers in Beijing are expected to maintain a targeted approach rather than resorting to broad-based stimulus.

EU growth remains subdued as Q3 GDP shows only modest improvement

EU GDP edged up 0.2% quarter-on-quarter in the third quarter, in line with expectations but still reflective of a sluggish growth environment. Annual growth slowed to 1.4%, pointing to persistent headwinds across the bloc.

Investment remains soft, industrial output is weak, and external demand continues to drag on performance. While some smaller member states show signs of resilience, several of the larger economies continue to struggle to gain traction. For policymakers, the data reinforces the need for ongoing support measures while avoiding heavy-handed stimulus.

Japan's economy contracts in Q3 as external pressures weigh on growth

Japan's economy slipped into contraction in the third quarter, with preliminary data showing GDP falling 0.4% quarter-on-quarter and declining 1.8% on an annualised basis. While both readings came in slightly better than expectations, they mark the first economic downturn in six quarters and highlight a weakening growth environment.

The decline was driven largely by external factors, including a sharp drop in exports following new U.S. tariffs that hit key manufacturing sectors such as autos. Housing investment also softened, adding to the drag from trade. Although domestic demand showed some resilience, supported by modest gains in private consumption and capital expenditure, it was not enough to counterbalance the external headwinds.

The latest figures reinforce concerns that Japan's recovery remains fragile. With underlying momentum slowing, economic authorities face a delicate balancing act as they assess whether this contraction signals a temporary setback or a more prolonged period of softness heading into the year's final quarter.

Week's Overview

Source: Investing.com

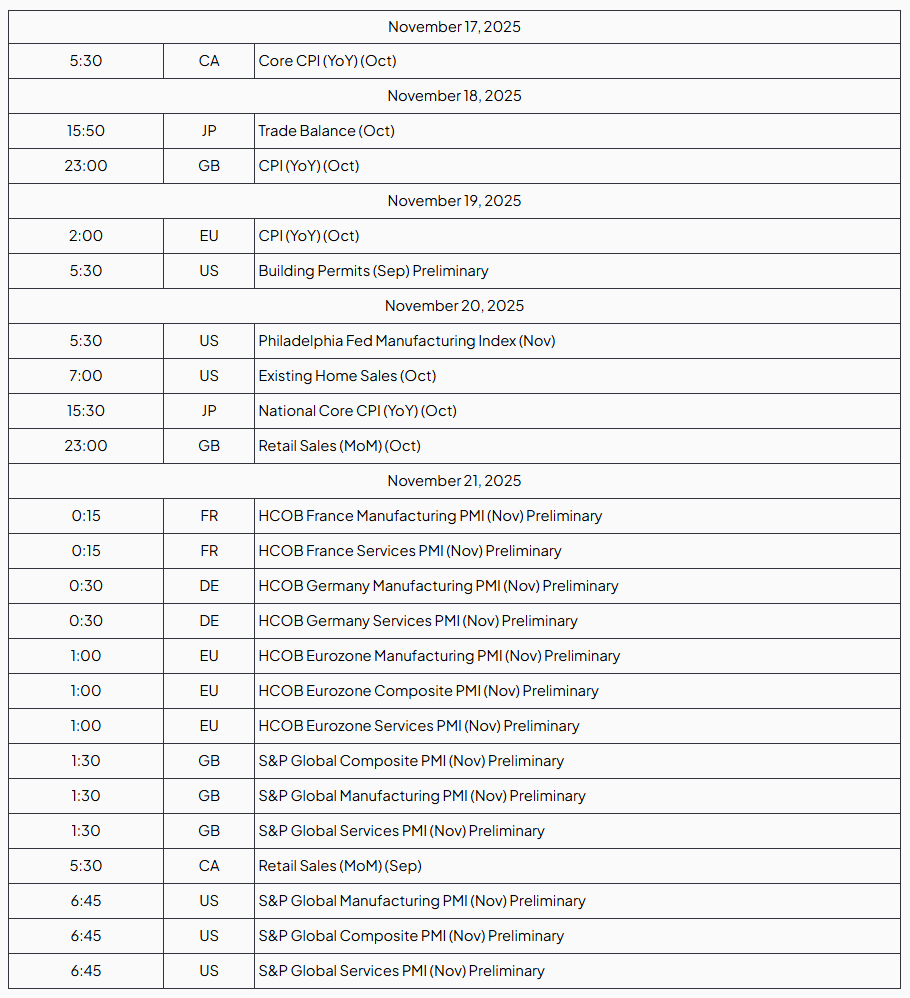

The Week Ahead

Next week, market attention will turn to fresh inflation readings from the U.K. and the Eurozone, offering updated insight into price pressures across major economies. In the U.S., investors will closely watch the release of the FOMC Meeting, alongside key activity indicators such as the Philadelphia Fed Manufacturing Index and Existing Home Sales. Toward the end of the week, PMI figures for both U.S. manufacturing and services will provide an important read on economic momentum heading into year-end.

Source: Investing.com Time: (GMT/UTC - 8h)

Regulation Environment

U.S. shutdown deal lifts market uncertainty as crypto sector eyes regulatory restart

The agreement reached in Washington to end the prolonged U.S. government shutdown is helping ease market uncertainty across both traditional and digital-asset markets. With federal agencies set to resume normal operations after more than six weeks of disruption, investors expect a clearer regulatory environment heading into early 2026.

The shutdown had frozen several key touchpoints for the crypto industry, including delayed rulemaking, paused enforcement actions, and slowed approvals for crypto-related financial products. The funding deal, extending government operations through January 30, 2026, allows agencies such as the SEC, CFTC and Treasury to restart pending reviews and compliance processes that had stalled during the closure.

Crypto analysts note that the reopening could accelerate timelines for ETF decisions, stablecoin guidance, and broader digital-asset policy discussions that were effectively on hold. While another funding debate looms early next year, the shutdown's resolution removes a major near-term overhang for markets and restores needed stability for both institutional and retail crypto participants.

Brazil's central bank finalizes crypto rules set to take effect in February 2026

The Banco Central do Brasil has approved a new regulatory framework for virtual-asset service providers, with rules scheduled to take effect on February 2, 2026. The framework, outlined in Resolutions 519, 520 and 521, requires crypto exchanges, custodians and brokers operating in Brazil to obtain authorization from the central bank, bringing the sector under formal financial supervision for the first time.

Under the new rules, transactions involving stablecoins and other virtual assets linked to fiat currency will be treated as foreign-exchange operations, subjecting them to the same oversight applied to traditional FX activities. The regulations also introduce heightened standards for governance, transparency, anti-money-laundering controls and information security.

Companies already active in Brazil will have a transition period until November 2026 to achieve full compliance. The move represents a major step in integrating digital-asset services into Brazil's broader financial regulatory system while tightening controls on cross-border crypto activity.

Figure brings YLDS to Solana, expanding real-world asset utility in DeFi

Figure is introducing YLDS, a registered public debt security, to the Solana blockchain, marking a significant step in bringing regulated real-world assets into the DeFi ecosystem. YLDS will be minted natively on Solana and is designed to provide continuous yield backed by U.S. Treasuries and Treasury repo agreements.

By issuing YLDS directly on Solana, Figure enables ecosystem partners to access a dollar-pegged, yield-bearing asset that integrates seamlessly with existing DeFi applications. Exponent Finance has been announced as the first partner to support YLDS, with additional collaborations planned to broaden access to tokenized real-world assets across Solana.

The launch strengthens Solana's position as a growing hub for institutional-grade DeFi, expanding the range of compliant assets available to developers and users across the network.

21Shares launches first U.S. crypto index ETFs under the SEC's 1940 Act

21Shares has introduced the first U.S. crypto index exchange-traded funds (ETFs) registered under the Investment Company Act of 1940, bringing a higher level of regulatory oversight to diversified digital-asset investing. The new products, the 21Shares FTSE Crypto 10 Index ETF (TTOP) and the 21Shares FTSE Crypto 10 ex-Bitcoin Index ETF (TXBC), track indexes developed by FTSE Russell and provide broad, rules-based exposure to major cryptocurrencies

Registration under the 1940 Act places these ETFs within the same regulatory framework used for traditional mutual funds and ETFs, imposing stricter standards on governance, custody, and investor protections. By using this structure, 21Shares aims to give both retail and institutional investors a more transparent and regulated way to access a diversified basket of digital assets through a single ticker

SoFi becomes first U.S. chartered bank to let customers buy crypto directly, including Solana

SoFi has launched a new in-app crypto trading service that allows its 12.6 million customers to buy digital assets, including Solana, directly from their bank accounts without using an external crypto exchange. Announced on November 11, 2025, the rollout makes SoFi the first nationally chartered U.S. consumer bank to offer integrated crypto trading to retail users

Through the new feature, customers can purchase, sell and hold cryptocurrencies using funds from their FDIC-insured checking or savings accounts, streamlining access to digital assets within a fully regulated banking environment. The launch is part of SoFi's broader push to expand digital finance offerings, bringing mainstream, bank-level accessibility to crypto markets

Canary Capital launches first U.S. spot XRP ETF

Canary Capital has officially launched its spot-XRP exchange-traded fund (ETF), trading under the ticker XRPC on Nasdaq. The product gives traditional investors direct exposure to XRP without needing to use crypto exchanges or self-custody wallets, a significant step forward for alt-coin-based financial products in the U.S

The ETF debuted with $58 million in first-day trading volume, the highest of any ETF launched in 2025, signaling strong demand from institutional and retail investors.

Transak secures six new U.S. state licenses, expanding stablecoin and fiat-to-crypto services to 11 states

Transak has expanded its regulatory footprint in the United States after securing Money Transmitter Licenses in six additional states: Iowa, Kansas, Michigan, South Carolina, Vermont and Pennsylvania. With these approvals, the company is now licensed to operate in a total of 11 states, enabling it to directly provide stablecoin transactions and fiat-to-crypto services without relying on intermediaries.

The new licenses allow Transak to broaden access to compliant digital asset on-ramps, supporting its strategy to build regulated payment infrastructure for users and businesses across the country.

SEC issues new guidance to accelerate ETF approvals, clearing backlog after shutdown

The U.S. Securities and Exchange Commission has released updated guidance allowing issuers to speed up the effectiveness of their registration filings, a move aimed at clearing the backlog that built up during the government shutdown. Under the change, issuers that filed without a delaying amendment can now have their registration statements automatically become effective after 20 days, and those seeking faster action may request acceleration under Rule 461.

The shift is expected to streamline reviews across a wide range of products, including several pending crypto-related ETFs. Market analysts say the new process could fast-track approvals for offerings tied to digital assets, reducing procedural delays and bringing greater clarity to issuers waiting for regulatory clearance. The updated guidance marks a notable step in restoring normal regulatory operations and reopening the pipeline for new ETFs to reach the market.

IRS reaffirms crypto is treated as property; gifts over $19,000 in 2025 require Form 709

The IRS has reiterated that digital assets, including cryptocurrencies, are treated as property for federal tax purposes, meaning they are not taxable to the recipient when transferred as a bona fide gift. Under the 2025 tax guidelines, individuals may gift up to $19,000 per recipient without triggering additional reporting requirements.

If the value of gifted crypto exceeds that amount, the donor must file Form 709, even if no tax is ultimately owed. Tax professionals emphasize the importance of accurate documentation, including fair-market value at the time of transfer and cost basis, to ensure proper reporting. The clarification reinforces existing rules while highlighting the need for careful recordkeeping as crypto usage continues to expand.

U.S. Senate introduces draft bill to expand CFTC authority over crypto markets

Lawmakers on the Senate Agriculture Committee have introduced a draft bill that would significantly expand the regulatory authority of the Commodity Futures Trading Commission (CFTC) over digital assets. The proposal would grant the agency direct oversight of spot trading in digital commodities, establish federal standards for crypto custody, and require trading platforms to register with the CFTC.

The bill aims to create a clearer regulatory framework for crypto markets by defining the CFTC as the primary supervisor for non-security digital assets, an area often marked by jurisdictional uncertainty between the CFTC and the SEC. If enacted, the legislation would bring exchanges, brokers and custodians under enhanced federal scrutiny, potentially reshaping compliance requirements across the industry.

The draft reflects growing bipartisan interest in strengthening market stability and consumer protections while reducing regulatory ambiguity. It signals a shift toward a more structured federal approach to crypto oversight, with the CFTC poised to play a larger role in governing the U.S. digital-asset ecosystem.

Technology and Innovation

OKX expands access to Solana ecosystem tokens through its mobile DEX

OKX has expanded support for the Solana ecosystem by enabling users to trade a wide range of Solana-based tokens directly through the OKX mobile decentralized exchange (DEX). The update allows app users to access and swap Solana tokens without relying on bridges or paying separate gas fees, streamlining participation in the broader Solana ecosystem.

The enhanced integration connects OKX's user base with a large collection of Solana network assets through a single interface, offering faster token discovery and simplified trading across multiple chains. While social media posts have highlighted the scale of access, OKX's DEX update primarily emphasizes multi-chain functionality and improved token availability for users seeking seamless decentralized trading.

Coinbase launches new token-sales platform for retail investors and issuers

Coinbase has announced the launch of a new token-sales platform, marking the company's return to primary token offerings for retail investors. The platform is designed to give verified users early access to new digital-asset launches while providing issuers with a regulated distribution channel for debuting their tokens.

The first sale hosted on the platform will feature MON, the native token of Monad Labs, offered during a one-week subscription window. Purchases are settled in USDC, and allocations prioritize smaller bids to encourage broad retail participation. Founders and affiliates of issuing projects will also be subject to a six-month lock-up period, strengthening transparency and investor protections.

With this initiative, Coinbase aims to streamline the process for token issuers while reopening a structured, compliance-focused path for retail users to participate in early-stage crypto projects.

Cash App to integrate Solana for USDC payments, expanding crypto functionality for millions of users

Cash App has announced plans to enable stablecoin payments using USDC on the Solana blockchain, with the rollout slated for early 2026. The upgrade will give each user a Solana-based blockchain address, allowing them to send and receive USDC directly from the app. Incoming USDC will automatically convert to U.S. dollars, while outgoing dollar transfers will be settled as USDC on Solana.

The decision to use Solana as the first supported blockchain highlights its speed and low transaction costs, making it suitable for everyday payments in a mainstream consumer application. By bringing Solana-based stablecoin transfers to its large user base, Cash App is positioning crypto not just as an investment product, but as an efficient payment rail integrated into a popular mobile finance platform.

Visa launches pilot enabling U.S. businesses to fund payouts in fiat while recipients receive stablecoins

Visa has introduced a new pilot program through Visa Direct that allows U.S. businesses to fund outgoing payments in fiat currency, while recipients can opt to receive those payouts in stablecoins directly into their crypto wallets. The initiative is aimed at creators, freelancers and gig-economy workers who often navigate slow or costly cross-border payment systems.

By settling payouts in dollar-backed stablecoins such as USDC, recipients gain faster access to funds and the ability to use or transfer them immediately on-chain. Visa is running the pilot with select partners ahead of a broader rollout, positioning the effort as a step toward bridging traditional payment rails with emerging blockchain-based financial infrastructure.

Standard Disclaimer: This report is provided for informational purposes only and does not constitute legal, financial, or investment advice. The views expressed represent the author's perspective at the time of publication and may change as market conditions develop. Although the information is drawn from sources deemed reliable, its accuracy and completeness are not guaranteed. Readers should exercise their own judgment and perform due diligence before making any decisions based on this report.

Contributors

Ana CabaleiroFinancial Analyst